In This Article

- The Economics of Lending Technology Ecosystems

- Three Pillars: CRM, POS, and LOS Integration

- ABT MortgageExchange: The Integration Spine for Lending

- Automation That Cuts Cost Per Loan

- Verification Intelligence: Where the Biggest Savings Hide

- Architecture That Scales Without Proportional Cost

- The KPI Framework That Drives Continuous Improvement

- Mortgage BI: Cost-to-Originate and Pipeline Visibility

- The M365 Guardian Operating Model

- Implementation Sequence: Where to Start for Maximum ROI

- Frequently Asked Questions

The Mortgage Bankers Association reported that total loan production expenses reached $11,076 per loan in 2024. That number has climbed steadily for three years running, and lenders with fragmented technology stacks are absorbing the worst of it. STRATMOR Group data shows that lenders using disconnected systems face per-loan costs up to 30% higher than peers with integrated platforms.

The gap between high-performing lenders and everyone else is widening. Freddie Mac research confirms that lenders using digital mortgage processes spend $2,200 less per loan than those relying on manual workflows. High adopters of automation save an additional $1,500 per loan beyond that baseline. These are not theoretical projections. They are measured cost differences between lenders operating on connected ecosystems and lenders still patching together disconnected tools.

This playbook covers how banks, credit unions, and mortgage companies build a lending technology ecosystem that reduces cost per loan, scales with volume changes, and delivers measurable operational improvements. It walks through the core technology pillars, the integration architecture that ABT MortgageExchange provides as a mortgage-aware spine, the automation priorities, the Mortgage BI overlay that surfaces cost-to-originate and pipeline visibility, the M365 Guardian operating model that governs the whole stack, and the implementation sequence that produces the fastest return.

The Economics of Lending Technology Ecosystems

Technology spending represents 5-10% of total loan production expenses, roughly $500 to $1,000 per loan according to STRATMOR Group benchmarks. That is a relatively small investment compared to the personnel costs, compliance overhead, and operational inefficiencies it can eliminate.

The math works like this: a lender processing 2,000 loans per year that reduces cost per loan by $1,500 through technology integration saves $3 million annually. The technology investment itself represents a fraction of that return. The issue is never whether technology pays for itself. The issue is whether the technology works as a connected system or as isolated tools that create their own overhead.

Connected ecosystems produce measurable advantages across three dimensions:

- Speed. ICE Mortgage Technology data shows integrated platforms reduce cycle times by 3 days on average. Freddie Mac's Loan Product Advisor update shortened production cycles by 5 days while qualifying 18,000 additional borrowers.

- Accuracy. ICE reports a 13% reduction in error rates for lenders using integrated platforms. Fewer errors mean fewer repurchase demands, fewer compliance findings, and less rework.

- Profitability. ICE data shows integrated lenders increase gross profit per loan by $1,056. That improvement comes from reduced labor per file, fewer fallout loans, and faster pull-through rates.

The economic case for integration is clear. The challenge is building the connections in the right order, which is what the rest of this playbook covers.

Three Pillars: CRM, POS, and LOS Integration

Every lending technology ecosystem rests on three core systems. The CRM manages relationships and pipeline visibility. The POS captures borrower data and documents at the point of application. The LOS processes the loan through underwriting, compliance, and closing. When these three systems share data through API connections, the entire operation accelerates.

CRM: Pipeline Visibility and Borrower Lifecycle Management

A connected CRM eliminates the information gaps that slow down loan officers. When a borrower submits a pre-qualification through the POS, the CRM captures that activity automatically. When the loan moves to processing, the CRM updates the pipeline stage without manual input. When the loan closes, the CRM triggers post-close nurture sequences that feed the referral pipeline.

Industry data shows that referrals drive approximately 40% of new mortgage business. A CRM that tracks every borrower interaction from first contact through post-close follow-up protects that revenue stream. The critical requirement is bidirectional data flow. The CRM should receive updates from the LOS and push relationship context back to loan officers working in the POS.

POS: Data Collection That Eliminates Downstream Rework

The POS determines the quality of every file that enters your pipeline. A well-designed POS collects verified data at the point of application through real-time credit pulls, income verification APIs, and document capture with OCR validation. When the POS delivers a complete, verified file to the LOS, processors work exceptions instead of chasing missing documents.

Research shows that lenders with integrated POS-to-LOS connections reduce processing time by 15-30 minutes per file on routine data transfer alone. Multiply that across thousands of loans and the labor savings are substantial.

LOS: The Processing Engine That Connects Outward

The LOS handles underwriting, compliance checks, third-party orders, and closing preparation. Modern LOS platforms connect to credit bureaus, appraisal management companies, title providers, and automated underwriting systems through API integrations that execute within the loan workflow.

The most effective LOS implementations treat the system as an integration hub rather than a standalone processing tool. Every third-party service connects through the LOS so data enters the ecosystem once and flows to every system that needs it. Freddie Mac data shows that automated underwriting through LPA returns decisions in minutes for standard profiles, and lenders using these integrations cut production cycles by 5 days on average.

ABT MortgageExchange: The Integration Spine for Lending

Banks, credit unions, and mortgage companies that try to build the three pillars from point-to-point feeds discover the maintenance burden compounds with every system added. Six systems mean roughly fifteen potential feeds. Each feed has its own monitoring, its own credentials, its own failure mode, and its own change management process. A schema change in the LOS vendor's quarterly release sends ripples through every feed that touches the LOS. The institution either staffs the maintenance burden or accepts feeds that go silently stale.

ABT MortgageExchange is the mortgage-aware integration spine that absorbs that burden. Pre-built connectors handle the POS, LOS, core banking system, servicing platform, and document management vendors that ABT customers actually run. The boarding event, escrow analysis event, payment posting event, and payoff event all map to mortgage-aware schemas by default. The audit trail is collected automatically, which matters when an examiner asks how a loan file moved from origination through boarding into the core.

Point-to-Point Integration

- Direct API or file feed from each source system to each target system

- Cheap to build for the first connection, expensive to maintain at scale

- Failure of one feed cascades across every system that depends on it

- Change management overhead grows quadratically with the number of systems

- Exam evidence requires reconstructing the path across every individual feed

Generic Middleware (ESB or iPaaS)

- Central hub routes messages between source and target systems

- One platform to maintain, with one schema to evolve

- Higher up-front cost, lower marginal cost per integration

- Vendor lock-in to the middleware platform

- Generic platform requires custom mortgage-specific mapping for every system

ABT MortgageExchange

- Pre-built connectors for LOS, core, servicing, and document management vendors

- Mortgage-specific data model preserved across every connection

- Boarding, payment posting, and escrow event handling included by default

- Microsoft Azure-hosted, monitored, and supported by ABT

- Audit trail and exam evidence collected by default, not bolted on

The LOS to core boarding feed is the highest-leverage integration MortgageExchange addresses. A loan boarded incorrectly creates a servicing exception that the next exam surfaces, a customer complaint that the next regulator complaint cycle surfaces, or a repurchase request that the next investor delivery cycle surfaces. Institutions that use MortgageExchange get the boarding event handling, field reconciliation, and audit evidence collection without building any of it. Our companion article on tracking the mortgage pipeline across systems covers the broader integration pattern in depth.

Automation That Cuts Cost Per Loan

Integration connects the systems. Automation eliminates the manual steps between them. The highest-value automation targets fall into three categories: document processing, workflow progression, and compliance enforcement.

Document processing automation. Intelligent document processing (IDP) uses OCR and machine learning to classify documents, extract data fields, and cross-reference extracted values against application data. When a borrower uploads a pay stub, the system reads the income figure, maps it to the loan file, and flags any discrepancy with the stated income on the application. Staff review exceptions rather than processing every document manually.

Workflow progression automation. Rule-based engines advance loans through pipeline stages when specific conditions are met. When verified income and assets exceed program thresholds, the system orders the appraisal automatically. When the appraisal clears, the system generates the closing disclosure. Each automated step removes a manual handoff and the delay that comes with it.

Compliance enforcement automation. TRID timing rules, fee tolerance calculations, and disclosure delivery requirements follow predictable logic. Automated compliance systems track every deadline, block actions that would create violations, and generate audit-ready documentation at every step. These automations prevent the most expensive errors in mortgage lending: tolerance cures that cost $500 to $2,000 per incident and regulatory findings that carry penalties orders of magnitude higher.

Freddie Mac data confirms that high adopters of automation save approximately $1,500 per loan. For a lender processing 3,000 loans per year, that translates to $4.5 million in annual cost reduction.

Verification Intelligence: Where the Biggest Savings Hide

Income and employment verification is one of the most labor-intensive steps in mortgage origination. Traditional verification requires phone calls to employers, faxed forms, and manual data entry. The process takes days and consumes significant staff time per file.

Automated verification platforms connect directly to employer payroll systems through APIs. Argyle, one of the leading verification platforms, reports a 55% average conversion rate on payroll connections and 88% cost savings per loan compared to traditional verification methods. The data flows directly into the loan file without manual entry, and the verification is timestamped and audit-ready.

The Work Number, Plaid, and similar services provide additional verification pathways. The most effective ecosystems support multiple verification sources and route each request to the provider most likely to return data for that specific employer. When the primary source fails, the system automatically tries secondary sources before falling back to manual verification.

Beyond cost savings, automated verification improves data quality. Payroll-connected income data is more accurate than borrower-reported figures, which reduces conditions, speeds underwriting, and lowers repurchase risk on the secondary market.

Architecture That Scales Without Proportional Cost

Mortgage volume is cyclical. Rate drops trigger refinance waves. Spring buying seasons spike purchase volume. A technology ecosystem that requires proportional staff increases for every volume change cannot deliver consistent margins.

Scalable architecture relies on three design principles:

- Cloud-first infrastructure. Cloud platforms scale compute and storage automatically with demand. Instead of purchasing server capacity for peak volume and paying for idle resources during slow periods, cloud infrastructure adjusts in real time. This approach reduces infrastructure costs by 30-50% compared to on-premises deployments.

- API-first design. When every system connects through documented APIs, adding new tools or replacing underperforming vendors does not require rebuilding the ecosystem. New integrations plug into existing data flows.

- Parallel processing capability. Automated workflows that run verification, appraisal, title, and compliance checks simultaneously instead of sequentially compress cycle times. When volume increases, parallel processing absorbs the additional load without creating sequential bottlenecks.

ICE Mortgage Technology data shows that lenders using integrated platforms achieve 23% higher operational leverage. That means they process more loans per employee without degrading quality or compliance. This operational leverage is the mechanism that allows integrated lenders to maintain margins during volume fluctuations.

The KPI Framework That Drives Continuous Improvement

An ecosystem that runs without measurement runs without direction. The following KPIs provide the feedback loop that identifies bottlenecks, validates investments, and drives continuous improvement.

Cost Per Loan

The MBA benchmark of $11,076 per loan is the industry average. Track your cost per loan monthly and compare it to your pre-integration baseline. Integrated ecosystems should show a declining trend as automation absorbs more manual steps. A reasonable target for a well-integrated lender is 10-15% below the MBA average within the first year of implementation.

Cycle Time (Application to Funding)

The industry average hovers near 43 days. Lenders with integrated ecosystems consistently close in 30-35 days. Track this metric by loan type and identify which stages consume the most time. Often, the bottleneck is not underwriting but document collection and verification, which is why automating those steps produces the largest cycle time improvements.

Processing Capacity Per Employee

This metric reveals whether your technology investment is creating operational leverage. If loans per processor per month increase without quality degradation, your ecosystem is delivering. If the number stays flat despite technology investment, the integration points between systems need attention.

Error Rate and Rework Percentage

Track the percentage of loans requiring rework due to data errors, missing documents, or compliance issues. ICE data shows a 13% reduction in error rates for integrated platforms. Each error avoided saves the cost of correction plus the opportunity cost of delayed closings.

Borrower Satisfaction and Application Completion Rate

Application abandonment rates reveal friction in the borrower experience. Post-close surveys measure the full journey. Together, these metrics show whether your ecosystem improvements are reaching the borrower or only benefiting internal operations.

Mortgage BI: Cost-to-Originate and Pipeline Visibility

The KPIs above only matter if the institution can see them. ABT Mortgage BI is the reporting and analytics overlay that surfaces cost-to-originate, pipeline visibility, channel performance, and operational outliers across the lending stack. Built on Microsoft Fabric and Microsoft Power BI inside the institution's Microsoft 365 tenant, it pulls from the LOS, the core banking system, the servicing platform, and the MortgageExchange event stream to produce a single rolled-up view that loan officers, branch managers, executives, and board members all work from.

The cost-to-originate view is the metric most institutions get wrong. Lenders that track production expense only at the institutional level miss where the cost actually lands. Mortgage BI breaks cost-to-originate down by channel, branch, loan officer, product, and pipeline stage, then benchmarks the result against the MBA Quarterly Performance Report. The institution that runs in the top quartile against the benchmark protects its margin through volume swings. The institution that runs above the benchmark identifies which channels, branches, and products are dragging the average and acts on the data before the next quarterly board meeting.

Pipeline visibility is the operational complement to cost-to-originate. Mortgage BI surfaces loans in each pipeline stage, the average days in status, files exceeding institutional SLA thresholds, the conversion rate at each pipeline gate, and the projected closing volume. Role-based dashboards tied to Microsoft Entra ID give branch managers a branch view, regional managers a regional rollup, and executives the institution-wide picture. Row-level security ensures each user sees only the data their role allows. Our BI implementation guide for financial institutions covers the broader business intelligence pattern that Mortgage BI sits inside.

The M365 Guardian Operating Model

The Microsoft 365 surface that supports the integration plane (Microsoft Entra ID for identity, Microsoft Purview for data governance, Microsoft Defender for Cloud Apps for SaaS visibility, Microsoft Sentinel for SIEM, Microsoft Fabric and Microsoft Power BI for analytics) provides an institution the tools. M365 Guardian is the operating model ABT runs on top of it for lending technology ecosystems. Guardian gives the institution the running configuration: Microsoft Sentinel analytics rules tuned to LOS-to-core boarding anomalies, escrow event volume spikes, and MortgageExchange feed latency thresholds; Microsoft Purview DLP policies calibrated to applicant NPI (Social Security numbers, income data, credit scores, loan amounts) flowing across the LOS, core, servicing, and document management surfaces; retention and audit policies aligned to FFIEC IT Examination Handbook, OCC Bulletin 2023-17, and NCUA examiner expectations for cross-system data flows, with retention durations and tamper-evident audit trails set the same way across every customer tenant; and 24/7 monitoring of those Sentinel and Defender signals, so a feed that silently fails at 2 a.m. is caught before the next morning's pipeline report tells the underwriting team the data is wrong. Banks, credit unions, and mortgage companies keep their Microsoft 365 licensing and retain their tenant ownership; the Guardian layer is added through ABT's partner relationship.

Implementation Sequence: Where to Start for Maximum ROI

Ripping out existing systems and starting over is rarely practical. The implementation sequence below prioritizes the changes that deliver the fastest measurable return.

Phase 1: Connect POS to LOS (Weeks 1-4). This single integration eliminates the most common source of manual data transfer. When borrower data flows from the POS to the LOS without re-keying, you immediately reduce processing time and data entry errors. Most major LOS platforms have API endpoints ready for POS connections.

Phase 2: Add document intelligence (Weeks 4-8). Layer OCR classification and data extraction onto your existing document upload workflow. This reduces document handling time by 6+ hours per loan and delivers the highest single-step labor savings in the pipeline.

Phase 3: Automate verification (Weeks 6-10). Connect to automated income and employment verification services. With 88% cost savings per verification reported by leading platforms, this step produces immediate and measurable cost reduction.

Phase 4: Build compliance automation (Weeks 8-14). Implement TRID timing enforcement, fee tolerance validation, and automated audit trail generation. These automations prevent the most expensive errors and reduce audit preparation from days to hours.

Phase 5: Integrate CRM, board MortgageExchange, and establish Mortgage BI dashboards (Weeks 12-16). Connect the CRM to receive pipeline data from the LOS and borrower activity from the POS. Stand up MortgageExchange as the integration spine for the LOS to core boarding feed. Build Mortgage BI dashboards on Microsoft Power BI that track the KPIs defined above. This phase completes the feedback loop that drives continuous improvement, and the M365 Guardian operating model layers on top to govern identity, data, and audit evidence across the stack.

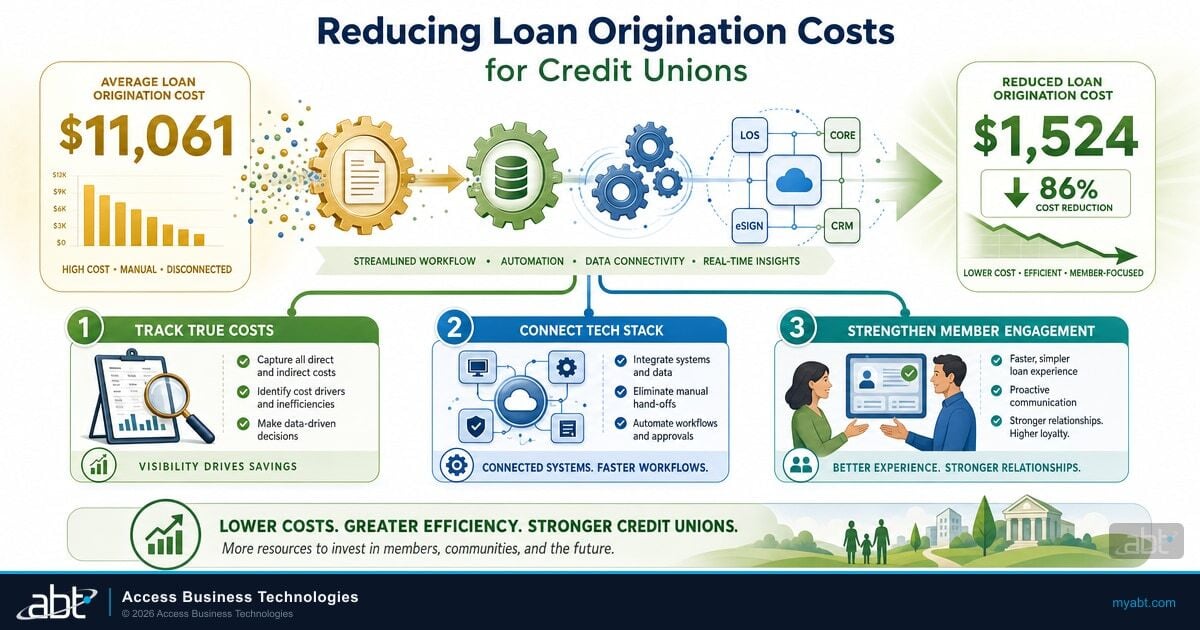

ABT helps banks, credit unions, and mortgage companies build connected lending ecosystems through this phased approach. We work with your existing CRM, POS, LOS, and core to create integrated workflows that eliminate manual handoffs and reduce cost per loan. See how cost compression plays out for credit unions in our companion guide on reducing loan origination costs for credit unions.

Ready to build a connected lending ecosystem?

Talk to an ABT specialist about ABT MortgageExchange, the Mortgage BI overlay on Microsoft Fabric and Microsoft Power BI, and the M365 Guardian operating model that together give banks, credit unions, and mortgage companies a single integrated lending stack with real-time pipeline visibility, cost-to-originate transparency, and audit-ready evidence by default.

Frequently Asked Questions

The MBA reports total mortgage loan production expense at $11,094 per loan for full-year 2025 and $11,102 per loan for Q4 2025. Lenders running fragmented stacks consistently land above that average; integrated lenders land below. Banks and credit unions running disconnected consumer-loan, commercial-loan, and deposit-origination systems see the same pattern in their non-interest expense ratios. Connected ecosystems also show 23% higher operational leverage in ICE Mortgage Technology data, which is the mechanism that protects margins through volume swings.

Connect your origination platform to your processing engine through API integration. For mortgage companies that means POS to LOS. For banks and credit unions that means digital banking and digital account-open to the core or to the consumer-loan origination workflow. This eliminates the most common source of manual data transfer and re-keying errors. Most major LOS, core banking, and digital banking platforms publish API endpoints ready for connection, and this single step saves processors 15 to 30 minutes per file on routine data handling.

Automated verification platforms connect to employer payroll systems through APIs, replacing manual phone calls, faxed forms, and data entry. Leading platforms report 60 to 80% verification cost reduction compared to traditional methods, 99% applicant search success rates, and 5 to 7 days cut from loan processing timelines. The data flows directly into the file, improving both speed and accuracy across mortgage, consumer-loan, and commercial-loan underwriting.

Microsoft 365 functions as the governance and identity control plane around the lending stack. Microsoft Defender for Cloud Apps surfaces unsanctioned SaaS connections to the LOS, core, or origination platform. Microsoft Purview classifies non-public personal information flowing between systems and enforces data-loss-prevention policies. Microsoft Entra ID Conditional Access requires phishing-resistant MFA and managed-device posture for vendor and employee access to loan data. Together these controls satisfy the third-party-risk-management expectations in the June 2023 Interagency Guidance and the FFIEC IT Examination Handbook for community banks and credit unions. ABT runs the M365 Guardian operating model on top of that surface for end-to-end lending governance.

ABT MortgageExchange is a mortgage-specific integration platform with pre-built connectors for the LOS, core banking, servicing, and document management vendors community banks, credit unions, and mortgage companies actually run. Generic middleware platforms provide a horizontal integration surface that any vertical can use, but every mortgage-specific data mapping, event handling routine, and audit evidence collection rule has to be built and maintained inside the platform. MortgageExchange ships with mortgage-aware schemas for boarding events, escrow analysis events, payment posting events, and payoff events by default, and the audit trail runs automatically. Institutions that choose generic middleware end up rebuilding mortgage logic that MortgageExchange includes by default.

Track five core metrics: cost per origination against the MBA mortgage benchmark or your internal baseline, cycle time from application to funding, processing capacity per employee, error rate and rework percentage, and applicant satisfaction with application-completion rate. Mortgage BI on Microsoft Power BI surfaces these metrics with role-based dashboards tied to Microsoft Entra ID identity. Together these reveal whether your technology investment is producing operational leverage and cost reduction across mortgage, consumer-loan, and commercial-loan books.

Yes. Most ecosystem improvements work alongside existing systems through API integration. Start by connecting the origination platform to the processing engine, then layer document intelligence and automated verification. Add compliance automation and CRM integration in later phases. Each step delivers standalone value without requiring a full LOS or core replacement, and most major LOS and core banking platforms expose API endpoints designed for exactly this kind of phased build. ABT MortgageExchange and the M365 Guardian operating model add the mortgage-aware integration spine and the governance layer without forcing a platform replacement.