In This Article

- Mortgage UX: What Borrowers Expect vs What Most Lenders Deliver

- The Three Pillars ABT Operates: Azure, API Management, and MortgageExchange

- The Latency Budget at Every Borrower Touchpoint

- Microsoft Azure Architecture for Low-Latency Mortgage UX

- Monitoring Real Borrower Experience with Azure Monitor and Application Insights

- Governance and Audit Evidence That Stands Up to Examiners

- The Bottom Line for Mortgage Lenders

- Frequently Asked Questions

A borrower in 2026 expects an online mortgage application to feel like ordering a car ride or transferring money between checking and savings. Tap, enter a few fields, see a confirmation. The mortgage industry has been trying to deliver that experience for a decade, and most lenders still cannot. McKinsey research shows borrower satisfaction with the mortgage process sits between 42 and 67 percent, with banks scoring 20 to 30 percentage points lower than non-bank originators. The gap is not a marketing problem. It is an infrastructure problem.

What looks like a slow website to the borrower is usually three or four backend systems failing to talk to each other in real time. The loan origination system waits on the pricing engine. The pricing engine waits on the credit bureau. The credit bureau response stalls at a network hop. The borrower watches a spinner and abandons the application. Speed is the visible symptom. The root cause is how the infrastructure, APIs, and latency budget are designed and operated.

This article walks through what mortgage borrowers actually experience at each touchpoint, where the infrastructure layer either delivers or breaks that experience, and how three things ABT operates — Microsoft Azure as the hosting platform, Azure API Management as the gateway, and MortgageExchange as the integration layer — deliver the response times borrowers expect while producing the audit evidence federal examiners require. The lender keeps tenant ownership of Microsoft 365; ABT runs the Azure environment as partner of record and adds the M365 Guardian operating model on top.

Mortgage UX: What Borrowers Expect vs What Most Lenders Deliver

Online mortgage banking inherits expectations from every other consumer fintech experience the borrower uses. They have just paid a bill in three taps, transferred funds in seconds, and checked a balance instantly. When the same borrower opens a mortgage application, they expect that pace to continue. Most lenders deliver something else.

The McKinsey work on borrower satisfaction identifies three specific pain points that drive low scores: delays in document upload and verification, slow turnaround on conditional approvals, and an inconsistent experience between mobile and desktop. Fannie Mae's research on the digital mortgage borrower confirms the pattern. Borrowers consistently rank ease of use and speed as the top two factors in choosing a lender, ahead of rate when the rate spread is within 25 basis points.

Borrowers in 2026 expect:

- Sub-second response to interactive actions. Clicking a field, opening a dropdown, advancing to the next page. Anything that feels like waiting for a server is friction.

- Document upload that completes in under five seconds for a typical pay stub or W2. Borrowers will retry once, then abandon if uploads stall.

- Real-time status visibility. Where am I in the process. What is the lender waiting on. When will I hear back.

- Mobile that behaves like the desktop. Starting on a phone and finishing on a laptop should feel like the same application, not two different products.

- Conditional approval within minutes when credit and income are clean. Not days. Not a callback from a loan officer.

Each of those expectations breaks down into a measurable infrastructure requirement. None of them are about the user interface. They are about how fast the systems behind the screen can talk to each other.

Why This Matters for Mortgage Lenders

The lender who delivers the experience above wins the borrower. In a market where 35 percent of repeat buyers select a lender within three days of starting their search, according to industry shopping behavior data, the first lender whose application loads fast and responds instantly often wins the loan before the second lender's branch even returns a phone call. Infrastructure is no longer a back-office concern. It is the front edge of the lender's competitive position.

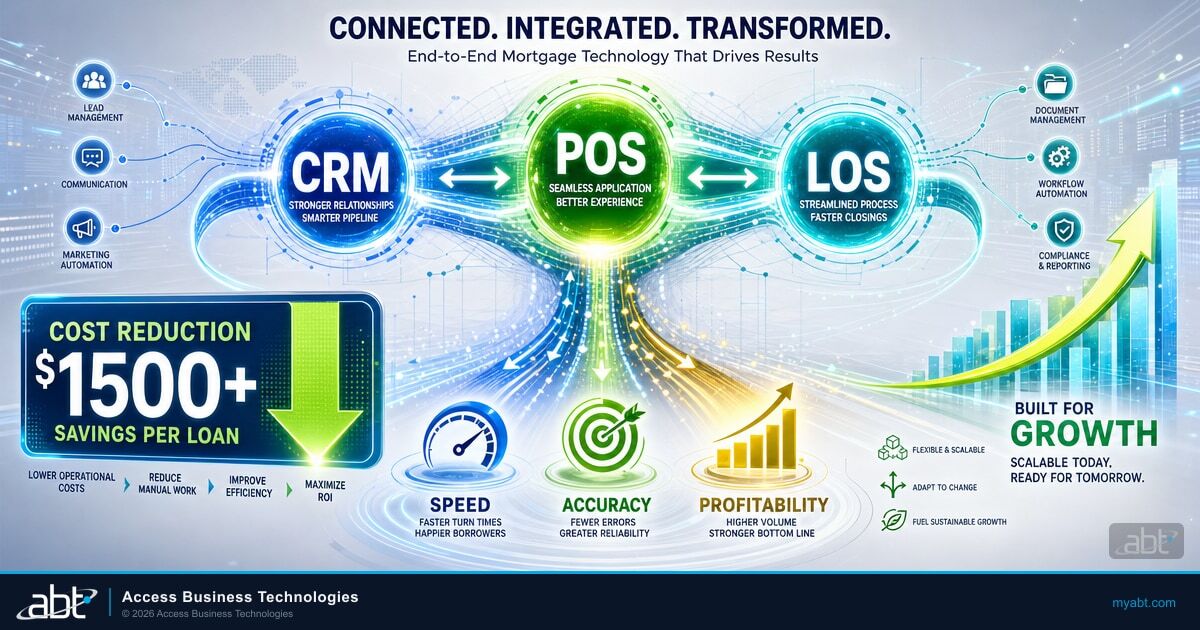

The Three Pillars ABT Operates: Azure, API Management, and MortgageExchange

Three pillars of the borrower-facing infrastructure are operated by ABT for the lender. Each one sits between the borrower's browser and the data that ultimately answers their question, and each one has a defined latency contribution that ABT measures and tunes. The lender retains tenant ownership of Microsoft 365; ABT runs the Azure environment as partner of record and absorbs the operational responsibility for keeping the three pillars inside the published latency budget.

Microsoft Azure — The Hosting Platform ABT Runs

ABT runs a dedicated Microsoft Azure subscription for each financial-institution customer as partner of record. The borrower-facing portal, the Calyx PointCentral mortgage workspace, custom mortgage applications, and the MortgageExchange integration layer all run inside that subscription. ABT selects the Azure region for proximity to the lender's branch footprint, configures geo-redundant storage for borrower documents, and applies the same Azure-hosted pattern across every customer environment so operational practice stays consistent. The lender keeps tenant ownership of Microsoft 365 and benefits from ABT's role as the Tier-1 Microsoft Cloud Solution Provider that operates the Azure compute, storage, and networking surface underneath.

Azure API Management — The Gateway ABT Runs For You

Azure API Management is the gateway that terminates and orchestrates every call to the loan origination system, the pricing engine, the credit bureau, and the core banking platform. ABT configures the gateway with rate-limit policies that protect the credit-bureau API budget during refinance waves, throttling rules that keep one LOS misbehavior from cascading into a portal outage, authentication enforced through Microsoft Entra ID for every borrower and every loan officer, and observability that feeds straight into Azure Monitor and Application Insights. The same gateway produces the per-request audit log examiners ask to see during an exam, with full timestamps, identities, and response codes. Without an API Management layer the lender's portal makes raw downstream calls and inherits every downstream failure mode without any policy buffer.

MortgageExchange — The Integration Layer ABT Runs

For institutions on ABT's MortgageExchange integration platform, the integration layer absorbs the protocol differences between the LOS, the servicing platform, the core banking system, and the document-management surface. Instead of point-to-point connectors that each have to be performance-tuned by the lender's own staff, MortgageExchange routes the traffic through a managed pipeline with consistent latency characteristics. The benefit at the UX layer is predictability: the borrower-facing portal can rely on one integration partner instead of stacking timeouts across three or four vendors. MortgageExchange supports 40+ mortgage technology systems — including Encompass, Calyx, Mortgage Cadence, Fiserv, Jack Henry, FIS, and Symitar — and uses mortgage-specific business rules to validate, transform, and route loan data. The ICE Mortgage Technology December 2026 deadline for migrating Encompass off its legacy software development kit and onto the modern API is a forcing function: every Encompass lender will be measuring LOS API performance through 2026, and MortgageExchange delivers real-time pipeline visibility across LOS, servicing, and core while the migration is underway.

The three pillars work together. Azure hosts the workload, API Management governs the traffic, and MortgageExchange normalizes the data flow. When any one of them is missing the borrower experiences the symptom even though the underlying problem is in a backend system the borrower never sees.

The Latency Budget at Every Borrower Touchpoint

A latency budget is a published target for how much time each step in a workflow is allowed to consume. Microsoft, Google, Amazon, and Cloudflare publish their own internal budgets. Mortgage lenders should publish theirs. The budget below reflects the targets Microsoft documents for Azure-hosted financial services applications, cross-referenced with Mortgage Tech Press analyses of borrower-portal performance data.

| Borrower Journey Stage | Latency Target | Primary Infrastructure Dependency | Failure Symptom |

|---|---|---|---|

| Login and authentication | 200 milliseconds | Microsoft Entra ID External Identities, Azure Front Door | Borrower retries password, suspects account is locked |

| Dashboard load after login | 800 milliseconds | Azure App Service, LOS API for loan-in-progress lookup | Borrower thinks the site is down |

| Form field interaction | 100 milliseconds | Azure Front Door CDN cache, client-side validation | Borrower types ahead and loses keystrokes |

| Loan application submission | 1.5 seconds | Azure Functions, LOS API write, core API identity match | Borrower hits submit twice and creates duplicate applications |

| Document upload (typical 2 MB file) | 2.5 seconds | Azure Blob Storage, virus scan pipeline, LOS document API | Borrower retries upload three times then abandons |

| Status check / pipeline view | 500 milliseconds | Azure App Service cache, LOS API read | Borrower calls the loan officer asking for status |

| Conditional approval response | 3 to 5 seconds (live), with async fallback | Pricing engine API, credit bureau API, automated underwriting | Borrower waits but does not abandon if progress is visible |

The numbers above are not aspirational. They are achievable on Microsoft Azure infrastructure with the architecture pattern described in the next section. The lenders who consistently miss these targets are usually running an older application stack on-premise, or running on Azure but without the edge caching, the connection pooling, and the observability that Azure makes available. These numbers are the contract ABT signs as the partner of record for the Azure environment.

Borrowers who experience a sub-1-second initial page load on the mortgage application portal are 2.3 times more likely to complete the application than borrowers experiencing a 3-second load. Borrowers experiencing a 5-second initial load complete at less than half the rate of the sub-1-second cohort.

Microsoft Azure Architecture for Low-Latency Mortgage UX

The architecture below is the pattern ABT runs for mortgage lenders on a dedicated Azure subscription. ABT hosts the customer's Azure environment as the partner of record, while Microsoft 365 identity is managed at the tenant level through Microsoft Entra ID. The four layers below are what ABT operates for you — the same Azure-hosted pattern ABT runs for Calyx PointCentral and for the custom mortgage applications its customers run alongside it. The combination delivers the latency budget above while producing the audit logs and security telemetry federal examiners expect.

Azure Front Door serves the borrower portal from the nearest edge location, terminating TLS, caching static assets, and routing dynamic traffic to the closest healthy backend.

Azure App Service runs the borrower portal application with autoscaling configured to handle rate-drop surges. Azure Functions handle event-driven workloads like document virus scanning and async credit pulls.

MortgageExchange routes LOS, servicing, and core banking traffic through a managed integration layer. Azure API Management governs every API call with rate limiting, authentication, and observability so refinance-wave volume never breaks the borrower portal.

Azure SQL Database holds session state and application metadata. Azure Blob Storage holds uploaded documents with encryption at rest. Connection pooling and read replicas keep query latency inside budget.

Each layer in this architecture has a specific latency contribution and a specific Microsoft Azure service responsible for it. The numbers in the latency budget table earlier are produced by tuning the four layers together.

The Azure services that move the needle on borrower experience are Azure Front Door for global edge caching, Azure App Service with autoscaling for the application tier, Azure Functions for asynchronous workloads that should never block the borrower, Azure Monitor and Application Insights for real-user telemetry, and Microsoft Entra ID for the authentication path. Stacking those services together produces a latency profile competitive with the largest non-bank originators, on infrastructure ABT operates as the partner of record. The Microsoft 365 tenant identity managed alongside the Azure environment is what produces the unified audit trail examiners expect.

How ABT Tunes the Four Layers for Mortgage Workloads

The Azure services above are the building blocks. ABT does the configuration work that turns them into a low-latency mortgage portal. At the edge, ABT sets Azure Front Door cache policies for portal static assets, brand fonts, and the application shell so the initial paint lands inside the 200-millisecond authentication target. At the compute layer, ABT writes App Service autoscale rules calibrated to rate-cut refinance-wave patterns so the portal absorbs 5x to 10x traffic without slowing the regular-volume borrower. ABT structures Azure Function async pipelines so credit pulls, income verification, and document virus scanning never block the borrower's screen — the borrower continues filling the application while the slow work runs in parallel and reports back when complete. At the integration layer, ABT tunes LOS API connection pools, applies Azure API Management throttling and authentication policies, and routes the resulting MortgageExchange traffic with documented latency budgets per downstream system. Each of these is a configuration decision, not a feature of Azure. The lender benefits from ABT having made the same decisions across more than 750 financial-institution environments.

Key Takeaway

A four-layer Azure architecture (Front Door at the edge, App Service for compute, Azure SQL and Blob Storage for data, and Azure API Management with MortgageExchange for integration) delivers the latency budget mortgage borrowers expect in 2026 while producing the audit telemetry federal examiners require. The infrastructure is operated as a managed service by ABT as the partner of record, which means the mortgage lender's IT team focuses on member-facing priorities rather than on autoscale rules and connection pool tuning.

Monitoring Real Borrower Experience with Azure Monitor and Application Insights

Latency targets that are not measured are not targets. They are aspirations. The architecture above is instrumented with Azure Monitor and Application Insights so that every page load, every API call, and every document upload is recorded with start time, end time, status code, and the user session identifier needed to reconstruct what an individual borrower experienced.

Application Insights provides three measurements that mortgage lenders should review weekly:

- Real-user page load time at the P95 percentile. The P50 average is meaningless when 1 in 20 borrowers is hitting a 10-second load. The P95 number is the number that matches what most abandoning borrowers experienced.

- API dependency response time, broken out by downstream system. When the LOS API slows down, the portal slows down. Application Insights shows exactly which downstream call is consuming the latency budget so the team can target the fix at the right system instead of guessing.

- Funnel conversion by load-time bucket. Comparing the application-completion rate of borrowers who experienced a sub-1-second initial load against borrowers who saw 3 seconds or more quantifies the revenue impact of latency. Mortgage lenders who present this number to the board usually receive infrastructure budget the following quarter.

Azure Monitor also feeds Microsoft Sentinel for security telemetry. The same signals that diagnose a slow page can flag a credential-stuffing attack against the borrower portal. ABT's managed Sentinel deployment is part of the M365 Guardian operating model — tuned for mortgage workload signal patterns, not generic Microsoft defaults — and correlates the Azure infrastructure signal with the Microsoft 365 identity signal coming from Entra ID, which is how the security team detects the difference between a slow borrower and a malicious one.

Governance and Audit Evidence That Stands Up to Examiners

Federal examiners (the OCC for national banks, the FDIC for state-chartered banks, the NCUA for credit unions, and the CFPB for mortgage compliance) expect documentation that the borrower experience meets the lender's published service-level commitments and that the technology decisions are traceable to a risk management framework. The architecture above produces the documentation by default.

Microsoft Purview audit logging captures who accessed which borrower record, when, and from where. The audit log is retained for the term the lender's compliance team specifies (typically 5 to 7 years for mortgage records) and is exportable for examiner review. Microsoft Entra ID Conditional Access policies document the authentication path for every borrower and every loan officer, including the multi-factor authentication requirements that satisfy NCUA Letter to Credit Unions 23-CU-04 and equivalent OCC and FDIC guidance. The same configuration pattern aligns with the same Encompass-and-Calyx audit overlay pattern ABT applies across its customer base.

The federal financial institutions reporting on cybersecurity also matters here. NCUA's annual cybersecurity report covering the period after the September 2023 incident reporting rule documents 892 cyber incidents filed between September 2023 and May 2024, and 1,072 incidents by August 2024, with roughly seven in ten involving a third-party vendor. The integration layer between an LOS and a core banking platform sits exactly in that third-party risk zone. A documented Azure architecture with Microsoft-native logging, identity, and integration controls produces the evidence examiners need to see that the third-party exposure is being managed deliberately rather than left to manual processes.

The Microsoft 365 and Microsoft Azure surface above is the baseline. M365 Guardian is the operating model ABT runs on top of that baseline for mortgage lenders. Guardian includes Microsoft Sentinel analytics rules tuned to the borrower-portal traffic patterns — credential-stuffing attempts, abnormal LOS API access from compromised loan-officer accounts, and MortgageExchange feed latency that signals a downstream system is failing. Guardian includes Microsoft Purview DLP policies calibrated to loan applicant nonpublic personal information (Social Security numbers, income data, credit scores, loan amounts) flowing across the LOS, core, servicing, and document-management surfaces. Guardian includes Microsoft Purview retention and audit policies aligned to FFIEC, OCC Bulletin 2023-17, and NCUA examiner expectations for cross-system data flows, with the same configuration applied consistently across every customer tenant. And Guardian includes 24/7 monitoring of the Sentinel and Defender signals, so a credential-stuffing attack at 2 a.m. is caught before the morning shift opens. Banks, credit unions, and mortgage companies keep their Microsoft 365 licensing and retain their tenant ownership; the Guardian layer is added through ABT's partner relationship. The result is borrower-portal latency targets that hold up through the next exam cycle, not just the next sprint.

The Bottom Line for Mortgage Lenders

Mortgage UX in 2026 is decided by infrastructure, APIs, and latency, not by the marketing budget or the loan officer's bedside manner. The borrower who experiences a sub-second login, an instant dashboard, a 1.5-second submission, and a 3-second conditional approval will choose that lender. The borrower who experiences slow page loads and timeouts will choose someone else, often within minutes of opening the application.

Three steps to close the gap:

- Publish your latency budget. Pick a target for each touchpoint. Make it visible to the engineering team, the loan operations team, and the executive team. What gets measured improves.

- Move the borrower portal to a Microsoft Azure environment hosted by ABT as partner of record. ABT runs the four-layer architecture (Front Door at the edge, App Service for compute, Azure SQL and Blob Storage for data, Azure API Management for gateway traffic, and MortgageExchange for LOS / POS / core / servicing integration) on a dedicated Azure subscription for your institution. The M365 Guardian operating model layers Sentinel, Purview, and 24/7 monitoring on top, so the latency gain is durable through the next exam cycle.

- Instrument with Azure Monitor and Application Insights. Review real-user P95 load time, API dependency response time, and funnel conversion by load-time bucket every week. Tie infrastructure decisions back to revenue, which is the only way infrastructure stays funded.

Get the borrower experience your competitors already advertise.

The Microsoft Azure environment hosted by ABT, the MortgageExchange integration layer, and the M365 Guardian operating model together deliver the latency budget your borrowers expect and the audit evidence your examiners require — operated as a managed service by the Tier-1 Microsoft Cloud Solution Provider trusted by more than 750 financial institutions.

Frequently Asked Questions

Sub-second initial page load, 200 milliseconds for authentication, 800 milliseconds for the dashboard after login, 1.5 seconds for application submission, and 2.5 seconds for a typical document upload. Borrowers in 2026 inherit expectations from every other consumer fintech experience, and the Akamai retail performance data summarized across Mortgage Tech Press industry coverage shows roughly a 7 percent conversion drop for every additional second of delay. The numbers are achievable on Microsoft Azure with Azure Front Door at the edge, Azure App Service for compute, Azure Functions for asynchronous work, and Azure API Management with MortgageExchange for integration.

ABT hosts the borrower-facing portal on Microsoft Azure as partner of record, delivering it from the global edge network through Azure Front Door, which terminates TLS in milliseconds and serves cached static assets without any round trip to compute. Azure App Service with autoscaling absorbs refinance-wave traffic spikes that would crash on-premise infrastructure. Azure Functions execute background workloads (virus scanning, credit pulls, income verification) asynchronously so they never block the borrower's screen. The combination produces sub-second response on interactive actions, which Akamai and Mortgage Tech Press research links directly to higher conversion rates.

Every borrower action eventually reaches the loan origination system through an LOS API call. For depository institutions, the core banking platform also receives identity and account-lookup calls during application start. The response time of those APIs sits directly on the borrower's screen, so slow downstream systems show up as slow pages even when the borrower portal itself is fast. ICE Mortgage Technology's Encompass platform has a documented December 2026 deadline for migrating from the legacy software development kit to the modern API, which makes LOS API performance a 2026 priority for every Encompass-based lender. ABT's MortgageExchange integration platform routes LOS, servicing, and core banking traffic through a managed pipeline with consistent latency characteristics.

Azure Monitor and Application Insights capture every page load, every API call, and every document upload with start time, end time, status code, and session identifier. The three measurements mortgage lenders should review weekly are real-user page load time at the P95 percentile, API dependency response time broken out by downstream system, and funnel conversion by load-time bucket. Comparing application completion rates between borrowers who experienced a sub-second load and borrowers who saw 3 seconds or more quantifies the revenue impact of latency in dollars per loan, which is what gets the infrastructure work funded.

Microsoft Purview audit logging captures who accessed which borrower record, when, and from where, retained for the term the lender's compliance team specifies, typically 5 to 7 years for mortgage records. Microsoft Entra ID Conditional Access policies document the authentication path for every borrower and every loan officer, including the multi-factor authentication requirements that satisfy NCUA Letter to Credit Unions 23-CU-04 and equivalent OCC and FDIC guidance. Microsoft Sentinel correlates the Azure infrastructure signal with the Microsoft 365 identity signal coming from Entra ID, producing the unified telemetry examiners expect to see. NCUA's annual cybersecurity report documents 892 cyber incidents filed between September 2023 and May 2024 and 1,072 by August 2024, with roughly seven in ten involving a third-party vendor, which makes documented integration controls a focal point of examinations.

MortgageExchange is the integration layer ABT runs on top of the Microsoft Azure environment it hosts for mortgage lenders, connecting loan origination systems, servicing platforms, and core banking systems through a single managed pipeline instead of through three separate point-to-point connectors. The benefit at the UX layer is predictability: the borrower portal can rely on one integration partner with documented latency characteristics, instead of stacking timeouts across three vendors. MortgageExchange supports 40+ mortgage technology systems and uses mortgage-specific business rules to validate, transform, and route loan data, which keeps the borrower-facing portal inside its latency budget even when the underlying systems vary in performance. Combined with Azure API Management as the gateway, MortgageExchange keeps the borrower portal inside its latency budget regardless of which underlying LOS, POS, core, or servicing system answers a given call.