In This Article

- Why the Core Conversion Left the LOS Behind

- What MortgageExchange Does (and Why It Exists)

- How Lafayette Federal Connected Calyx Path and KeyStone

- The Growing Wave of KeyStone Conversions

- Results That Compounded Over Time

- The Real Cost of Manual LOS-to-Core Processes

- What This Means for Core Modernization Planning

- Technical Reference

- Frequently Asked Questions

Lafayette Federal Credit Union had a problem most credit unions would recognize. The $2.15 billion institution had just finished converting to Corelation KeyStone, a modern core banking platform with open APIs and the kind of architecture that makes IT teams optimistic. But after months of planning, budget allocation, and staff training, the mortgage department was still retyping every closed loan by hand.

The culprit was Calyx Path, the credit union's loan origination system. Path and KeyStone didn't have a native connection. So every time a mortgage closed, someone on Lafayette Federal's team sat down and manually entered borrower data, loan terms, and servicing details into the core. The same data. Typed twice. With every keystroke introducing the possibility of a transposed digit, a misspelled name, or a field left blank.

Lafayette Federal, headquartered in Rockville, Maryland, serves over 57,000 members across 11 branch locations. The credit union celebrated its 90th anniversary in 2025 and has built a reputation for investing in technology that keeps pace with member expectations. The KeyStone conversion was part of that strategy. But until the LOS-to-core gap was closed, the mortgage team was stuck in a workflow that belonged to a previous decade.

Why the Core Conversion Left the LOS Behind

Credit unions often assume that moving to a modern core with open APIs will make third-party integration straightforward. Corelation KeyStone is built on exactly that promise -- an open architecture designed to connect with other platforms. But "possible" and "automatic" are different things.

The LOS vendor and the core vendor build their APIs independently. Different data models. Different field naming conventions. Different validation rules. KeyStone's open API makes the connection architecturally feasible, but someone still has to build and maintain the translation layer between the two systems.

Lafayette Federal's IT team had just spent months on the KeyStone conversion. They didn't have the bandwidth to build a custom LOS integration from scratch. And Calyx wasn't going to build it for them. So the staff became the middleware -- manually bridging the gap between two systems that were each supposed to make things easier.

The specific friction points were predictable:

- Duplicate data entry on every closed mortgage. Staff typed the same borrower information, loan terms, and servicing details into both Calyx Path and KeyStone.

- Delayed loan boarding. New mortgages didn't appear in member accounts until the re-keying was complete, sometimes days after closing.

- Transcription errors that required manual reconciliation, occasionally surfacing weeks later during compliance reviews.

- Compliance exposure when NCUA examiners found mismatched data between the LOS and core.

- Staff frustration as loan officers spent hours on repetitive data entry instead of member service and loan production.

The ROI on the KeyStone conversion was being quietly eroded every time someone sat down to retype a closed loan.

What MortgageExchange Does (and Why It Exists)

MortgageExchange is a cloud-managed integration platform built by Access Business Technologies (ABT) specifically for credit unions, banks, and mortgage companies running disconnected lending systems. It connects loan origination systems to core banking platforms, servicing software, and wire transfer systems through pre-built connectors and configurable business rules.

MortgageExchange is not generic middleware. It was designed for the specific data structures, regulatory requirements, and operational patterns of mortgage lending at financial institutions. The platform supports over 40 mortgage technology systems, including every major LOS, core banking platform, and servicing system in the credit union and community bank space.

Hosted on Microsoft Azure, MortgageExchange runs with encryption in transit and at rest, 99.9% uptime standards, and proactive monitoring. ABT manages the platform end-to-end -- the credit union's IT team doesn't maintain servers, write API code, or troubleshoot integration failures when a vendor releases an update.

How Lafayette Federal Connected Calyx Path and KeyStone with MortgageExchange

Lafayette Federal deployed MortgageExchange to create a direct, automated data pipeline between Calyx Path and Corelation KeyStone. Instead of asking staff to keep bridging the gap manually, the integration handled the entire post-closing data flow.

Here is what MortgageExchange delivered for Lafayette Federal:

- Automatic post-closing data transfer. When a loan closed in Calyx Path, MortgageExchange extracted the loan record, validated it against business rules, and posted it to KeyStone. No one retyped anything. The entire post-closing handoff became a background process.

- Bi-directional synchronization. Updates in KeyStone that affected the LOS flowed back automatically through MortgageExchange. Both systems stayed current without manual reconciliation. Any employee could trust either system as the source of truth at any time.

- Rules-based field validation. Every data point was checked against configurable business rules before crossing between systems. Only clean, verified records moved through the pipeline. If a field didn't match expected formats, MortgageExchange flagged it for review instead of pushing incorrect data forward.

- Cloud-hosted on Microsoft Azure. The integration ran with enterprise-grade security and redundancy. No on-premise servers to maintain or patch.

- Fully managed by ABT. Lafayette Federal's IT team didn't maintain the integration infrastructure. ABT handled compatibility adjustments, monitoring, and issue resolution as part of the managed service. When Corelation or Calyx released updates, ABT updated the MortgageExchange connectors.

The Growing Wave of KeyStone Conversions

Lafayette Federal is not the only credit union facing this exact scenario. Corelation signed 27 new credit unions for KeyStone conversions in 2025 alone -- seven in Q1, seven in Q2, and thirteen in Q3 -- with go-live dates stretching through 2027. The largest signing was Wings Credit Union, a nearly $20 billion institution formed through a merger-of-equals between Colorado and Minnesota's largest credit unions, with conversion scheduled for 2028.

Bay Federal Credit Union faced a similar disconnect after its Encompass deployment -- see how Bay Federal streamlined post-closing with MortgageExchange for a parallel pattern in the LOS-to-core gap.

Every one of those credit unions will face the same LOS integration question Lafayette Federal faced. KeyStone's open API architecture creates the foundation, but the LOS-to-core translation layer still needs to be built, maintained, and monitored by someone who understands both sides of the connection.

Credit unions that plan the LOS integration alongside the core conversion avoid the gap entirely. Those that defer it to "phase two" end up exactly where Lafayette Federal started: with a modern core and a mortgage team still retyping data by hand. For ABT's fuller take, see Breaking the Mortgage Data Bottleneck.

Results That Compounded Over Time

Manual re-entry stopped on day one. Staff no longer typed the same data twice. The hours they recovered went back to loan processing, member service, and new application intake.

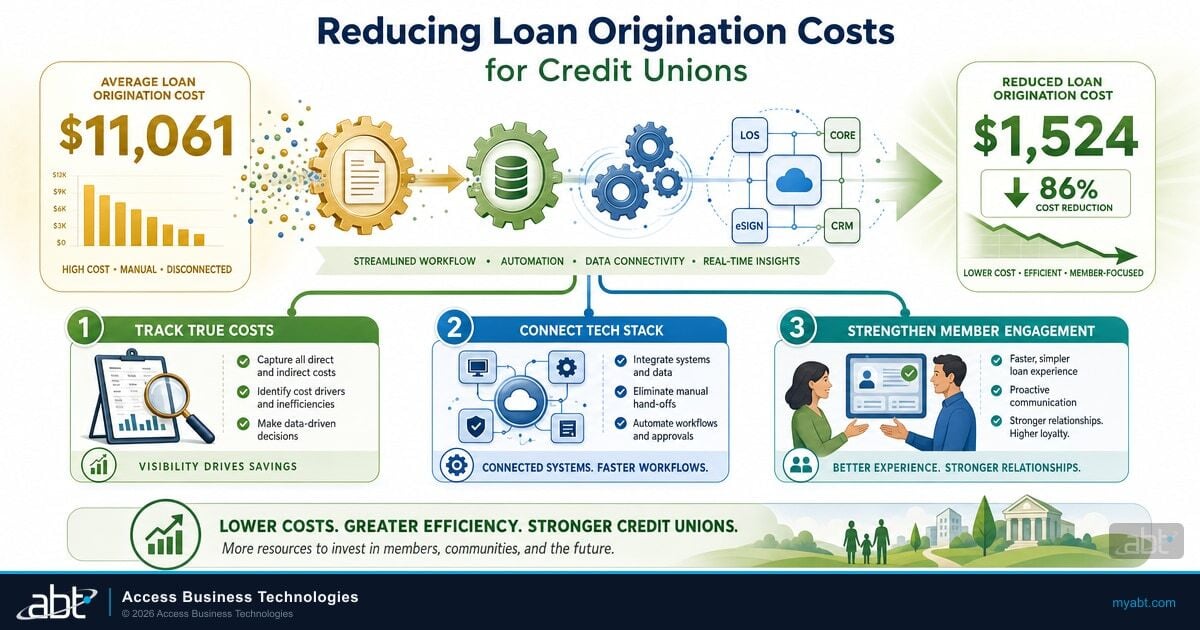

Data quality improved across the board. MortgageExchange's validation engine caught formatting errors, missing fields, and inconsistencies that manual re-entry had been introducing for years. Loan records matched across both systems from the moment of closing. This connects closely to Reducing Loan Origination Costs for Credit Unions.

Members noticed faster service. New mortgages appeared in online banking and member account screens within minutes of closing, not days. The "when will my mortgage show up?" calls to member service dropped significantly. See also our breakdown of Mortgage POS in 2026.

Compliance risk shrank. With identical data in both the LOS and core, Lafayette Federal could hand NCUA examiners a consistent set of records without spending days reconciling discrepancies. MortgageExchange's automated audit trail replaced the patchwork of manual logs that had covered the gap before. Every data movement was logged, timestamped, and traceable. For a deeper look at how integrated LOS data supports examination readiness, see Always Audit-Ready: Using Encompass and Calyx to Keep Compliance Locked Down.

The core conversion investment paid off fully. KeyStone's modern architecture was finally connected to every system that mattered, including the mortgage operation that generates some of the credit union's most complex and regulated data.

The Real Cost of Manual LOS-to-Core Processes

What makes this problem persistent is how effectively it hides. Executives see closed loan numbers on a dashboard. Board members review growth in quarterly reports. Members experience their mortgage closing as a milestone. Nobody sees the hours of clerical work happening behind the scenes to move that data from one system to another.

But the costs accumulate. Research from McKinsey found that financial institutions running legacy or disconnected systems face operating costs up to 10 times higher than those with integrated platforms. Most of that gap comes from manual processes: staff time, error correction, compliance remediation, and the opportunity cost of skilled employees doing work that software should handle. CFCU Community Credit Union saw the same hidden costs before MortgageExchange closed its data loop.

For credit unions specifically, the staffing math is straightforward. Loan officers who spend two hours per day on data re-entry aren't available for member consultations, pipeline management, or processing new applications. Over the course of a year, that adds up to roughly 500 hours per loan officer redirected from revenue-generating activity to clerical work. Multiply that across a mortgage team and the hidden cost becomes a line item that never appears in any budget.

Regulators don't care why the LOS and core show different numbers. They care that they do. A pattern of discrepancies between systems can escalate from a minor finding to a matter requiring attention during the next NCUA exam cycle.

What This Means for Financial Institutions Planning Core Modernization

The lesson extends beyond credit unions running Corelation and Calyx. Any financial institution upgrading its core banking platform needs to include LOS integration in the project plan from the start. A modern core with open APIs is a foundation, not a finish line.

For institutions running technology stacks from multiple vendors, MortgageExchange can connect LOS platforms, core banking systems, servicing software, and wire transfer systems through a single managed integration layer. ABT builds, hosts, and maintains those connections as an ongoing service -- a fundamentally different model from building custom integrations in-house, where every vendor update can break the connection.

ABT serves 750+ financial institutions as a cloud-first MSP and Tier-1 Microsoft CSP, with deep experience connecting lending systems across credit unions, community banks, and mortgage companies. MortgageExchange supports over 40 mortgage technology systems and is hosted on Microsoft Azure with enterprise-grade security and redundancy.

If your credit union is planning a core conversion, or if you already finished one and the mortgage team is still retyping data, the integration question isn't something you can push to next quarter -- and when ABT delivers MortgageExchange under the M365 Guardian operating model, the integration becomes part of a unified Microsoft 365 security, compliance, and management posture rather than another disconnected vendor tool. It is the difference between a technology upgrade and a technology transformation.

Technical Reference

The following terms appear in this article and are common in credit union and mortgage technology environments:

- MortgageExchange: ABT's cloud-managed integration platform that connects loan origination systems, core banking platforms, servicing software, and wire transfer systems through pre-built connectors and configurable business rules. Supports 40+ mortgage technology systems. Hosted on Microsoft Azure.

- Loan Origination System (LOS): Software used to process mortgage applications from intake through closing. Examples include Calyx Path, Calyx Point, ICE Mortgage Technology Encompass, and Black Knight Empower.

- Core Banking System: The central platform that manages a financial institution's accounts, transactions, and general ledger. Corelation KeyStone, Fiserv DNA, and Jack Henry Symitar are common credit union cores.

- Bi-Directional Synchronization: An integration pattern where data flows in both directions between connected systems, keeping all platforms current without manual reconciliation.

- Rules-Based Data Exchange: An integration approach where data transfers are governed by configurable business rules that validate, transform, and route information between systems before writing to the receiving platform.

Connect Your LOS and Core the Way Lafayette Federal Did

If your credit union runs Corelation KeyStone, Calyx Path, or any combination of LOS and core that requires manual re-entry after every closing, MortgageExchange can eliminate the gap. ABT manages the integration end-to-end as part of our M365 Guardian operating model, so your IT team doesn't write API code, patch servers, or chase vendor updates.

Frequently Asked Questions

MortgageExchange creates an automated data pipeline between Calyx Path and Corelation KeyStone using pre-built connectors and configurable business rules. When a loan closes in Path, MortgageExchange extracts the record, validates every field against business rules, and posts it to KeyStone without manual re-entry. The platform synchronizes data bi-directionally so both systems stay current.

Modern cores like KeyStone provide open APIs that make integration architecturally possible, but each vendor builds its API independently with different data models and field conventions. Someone still needs to build the translation layer that maps fields, validates data, handles exceptions, and maintains compatibility when either vendor releases updates. Without a platform like MortgageExchange, staff become the manual bridge.

MortgageExchange supports over 40 mortgage technology systems, including loan origination platforms like Calyx Path, Calyx Point, Encompass, and Empower, core banking systems like Corelation KeyStone, Fiserv DNA, and Jack Henry Symitar, servicing platforms, and wire transfer systems. The platform uses pre-built connectors with configurable validation rules for each system pair.

Corelation signed 27 new credit unions in 2025 alone, with conversions scheduled through 2027. The largest signing was Wings Credit Union, a nearly $20 billion institution formed through a merger-of-equals, with conversion set for 2028. Each converting credit union will need to address LOS-to-core integration as part of its KeyStone deployment plan.

ABT manages the entire MortgageExchange integration as an ongoing service, including platform hosting on Microsoft Azure, security and encryption, connector maintenance when vendors release updates, data validation monitoring, exception handling, and issue resolution. The credit union's IT team does not maintain servers, write API code, or troubleshoot integration failures.