Most credit unions run one type of mortgage program. One Nevada Credit Union runs two: traditional forward mortgages and specialized reverse mortgages for senior members. That means two origination platforms, one core banking system, one servicing platform, and a wire transfer system that connects to all of them. Five systems that need to share data reliably every time a loan closes.

In This Article

- One Nevada Credit Union: Five Systems, Two Mortgage Lines, One Goal

- The Cost of Disconnected Mortgage Systems

- How MortgageExchange Unified Five Systems Through One Integration Hub

- What Changed After MortgageExchange Went Live

- Why the MortgageExchange Pattern Matters Beyond One Nevada

- Building the Business Case for Credit Union Mortgage Integration

- Technical Reference

- Frequently Asked Questions

When those systems don't communicate automatically, staff members become the integration layer. They re-key borrower data from the origination system into the core. They manually board loans into the servicing platform. They type wire instructions into a separate transfer system. Every handoff is another chance for a typo, a transposed digit, or a missed field to cascade through the operation.

One Nevada decided to fix the root cause rather than keep adding workarounds. The credit union deployed MortgageExchange, a cloud-managed integration platform from Access Business Technologies (ABT), to connect all five systems through a single managed hub. The result: dual data entry eliminated entirely across both forward and reverse mortgage operations.

One Nevada Credit Union: Five Systems, Two Mortgage Lines, One Goal

One Nevada is the largest locally based credit union in Nevada. Headquartered in the Las Vegas metro area, it serves approximately 74,000 members across locations in Las Vegas, Henderson, Reno, and North Las Vegas, with over $1.5 billion in assets. The credit union celebrated its 75th anniversary in 2025 and was ranked number one nationally in American Banker's "Best Credit Unions to Work For" that same year.

One Nevada offers both forward mortgages (home purchases, refinances) and reverse mortgages (Home Equity Conversion Mortgages for senior members). This dual-program approach serves members at every life stage but creates operational complexity that most credit unions don't face. Each mortgage type runs on its own origination platform, and both need to connect to the same downstream systems for core banking, servicing, and funding.

The technology stack included five platforms:

- QuantumReverse -- a web-based reverse mortgage origination system for HECM loans.

- MeridianLink OpenClose -- the forward mortgage loan origination system for home purchases and refinances.

- Jack Henry Symitar (Episys) -- the core banking system managing member accounts and the general ledger.

- FICS MortgageServicer -- the servicing platform managing both forward and reverse mortgage loans post-closing.

- Fiserv WireXchange -- the wire transfer platform for funding disbursements.

Each system excelled at its job. None of them were built to talk to the others.

The Cost of Disconnected Mortgage Systems

The lack of integration between these five platforms created a predictable set of problems that will sound familiar to any financial institution running multiple best-of-breed systems.

Dual data entry at every handoff. When a reverse mortgage closed in QuantumReverse, staff had to manually re-enter the borrower and loan information into Symitar (to set up the loan account), into FICS (to begin servicing), and into WireXchange (to initiate funding). Forward mortgages closing in OpenClose required the same manual boarding into FICS. One loan could generate three or four separate re-entry events.

Errors that rippled across the operation. A transposed digit in a Social Security number entered into one system but not the others created a data mismatch that could surface during a regulatory examination. A misspelled name in the servicing system didn't match the core, which didn't match the origination file. Every manual entry point was an error injection point.

Lag between closing and operational readiness. Because data moved manually, there was always a delay between when a loan closed and when all systems reflected it. New borrowers couldn't access their loan information online until someone in the back office finished boarding the data. Reverse mortgage borrowers waiting for disbursement had to wait while wire instructions were typed and verified by hand.

Staff time consumed by clerical work. Mortgage and operations team members spent hours on data entry and cross-system reconciliation instead of advising members or processing new applications.

Bill Gibson, One Nevada's VP of Mortgage Servicing, framed the challenge simply: the credit union was "dedicated to providing our members with the most up-to-date service and technology available" -- but the manual processes between systems were holding them back.

How MortgageExchange Unified Five Systems Through One Integration Hub

One Nevada deployed MortgageExchange to act as a central data hub between all five systems. Rather than building direct connections between each pair of platforms (which would have required ten separate integrations), MortgageExchange functions as a unified integration platform that handles translation and routing across every connected system.

Each system connects to MortgageExchange once. MortgageExchange handles data transformation, validation, and routing to every other connected system. This approach is standard in enterprise integration, but MortgageExchange is purpose-built for the specific data structures and regulatory requirements of mortgage lending at financial institutions. The platform supports over 40 mortgage technology systems and is hosted on Microsoft Azure with enterprise-grade security.

MortgageExchange was configured to address four specific integration points at One Nevada:

Reverse Mortgage Funding: QuantumReverse to Fiserv WireXchange

When a reverse mortgage is ready to fund, MortgageExchange extracts the borrower's wiring instructions, loan amount, and disbursement details from QuantumReverse and pushes them directly into WireXchange. The wire system receives validated, formatted data ready for review and Fedwire transmission. No one re-types routing numbers or account details. The audit trail captures every data element that moved between systems and when.

For senior members waiting on reverse mortgage proceeds, this means faster access to their funds with fewer errors in the disbursement process.

Core Banking Updates: QuantumReverse to Jack Henry Symitar

MortgageExchange automatically boards new reverse mortgage loans into Symitar after closing. It creates member records if the borrower is new, posts the loan to the general ledger, and updates account balances -- all without manual intervention. The system checks whether the member already exists in the core before creating duplicates, which prevents the record fragmentation that plagues institutions with disconnected systems.

Reverse Mortgage Servicing: QuantumReverse to FICS MortgageServicer

All reverse mortgage loan data -- balances, rates, amortization schedules, escrow information -- transfers directly from QuantumReverse to the servicing platform through MortgageExchange. One Nevada can begin servicing a reverse loan immediately upon closing, with complete and accurate data in FICS from day one. Members can access their loan details through the online servicing portal right away, rather than waiting days for manual boarding to complete.

Forward Mortgage Servicing: MeridianLink OpenClose to FICS MortgageServicer

Forward mortgages follow the same automated path through MortgageExchange. When a home purchase or refinance closes in OpenClose, the loan setup details push into FICS through MortgageExchange with built-in validations that check for completeness and format consistency. The servicing team no longer waits for spreadsheets or closing packages to manually board new loans. New homeowners can set up their first payment or view their loan information online immediately after closing.

What Changed After MortgageExchange Went Live

The integration eliminated the operational drag that had been limiting One Nevada's mortgage operations:

- Dual data entry eliminated entirely. Staff stopped re-typing loan data across QuantumReverse, OpenClose, Symitar, FICS, and WireXchange. MortgageExchange handles all data movement between systems. The hours previously consumed by repetitive entry are now available for member-facing work.

- Data accuracy across all platforms. With data flowing directly from system to system through MortgageExchange's validated rules, the transcription errors that used to arise from manual input were effectively removed. Consistent data across all five platforms means cleaner regulatory reports and fewer examiner findings.

- Faster funding and servicing onboarding. Reverse mortgage borrowers receive their funds faster through automated wire initiation. Forward mortgage borrowers see their loan details online immediately after closing. The lag between closing and operational readiness dropped from days to hours.

- Staff redirected to advisory work. Mortgage and operations teams transitioned from data entry to member advising. The credit union's team can handle greater volume without proportional headcount increases.

- Compliance posture strengthened. When all systems agree on loan details, NCUA examinations go smoother. MortgageExchange creates audit trails for every data transfer, documenting what moved, when, and what validation rules were applied.

Why the MortgageExchange Pattern Matters Beyond One Nevada

One Nevada's mortgage integration challenge is not unique to credit unions. Community banks running separate LOS and core platforms face the same dual-entry problem. Mortgage companies managing multiple origination channels through different systems encounter the same data consistency issues. CFCU Community Credit Union solved the same disconnect with MortgageExchange, and any financial institution running best-of-breed platforms from different vendors has some version of this problem.

The MortgageExchange unified integration platform offers several advantages that apply across institution types:

- Vendor independence. Each system connects to MortgageExchange, not directly to other systems. If One Nevada replaced OpenClose with a different LOS, only the MortgageExchange connector to that system would need updating. Every other integration continues to work. Lafayette Federal connected Corelation Keystone with Calyx Path the same way.

- Scalability without complexity. Adding a sixth system to the stack requires one new MortgageExchange connector, not five point-to-point integrations. As institutions add platforms -- CRM systems, document management, investor delivery -- the integration cost grows linearly, not exponentially.

- Regulatory alignment across frameworks. Whether the institution answers to NCUA (credit unions), the OCC (banks), or state regulators and the FTC Safeguards Rule (mortgage companies), the expectation is the same: consistent, accurate data across all systems of record. MortgageExchange enforces that consistency automatically.

- Cloud-native deployment. MortgageExchange runs on Microsoft Azure with encryption in transit and at rest. There is no on-premises hardware to maintain. ABT manages platform upkeep, security patching, and monitoring as part of the service. Bay Federal Credit Union streamlined post-closing with the same managed-service model.

Building the Business Case for Credit Union Mortgage Integration

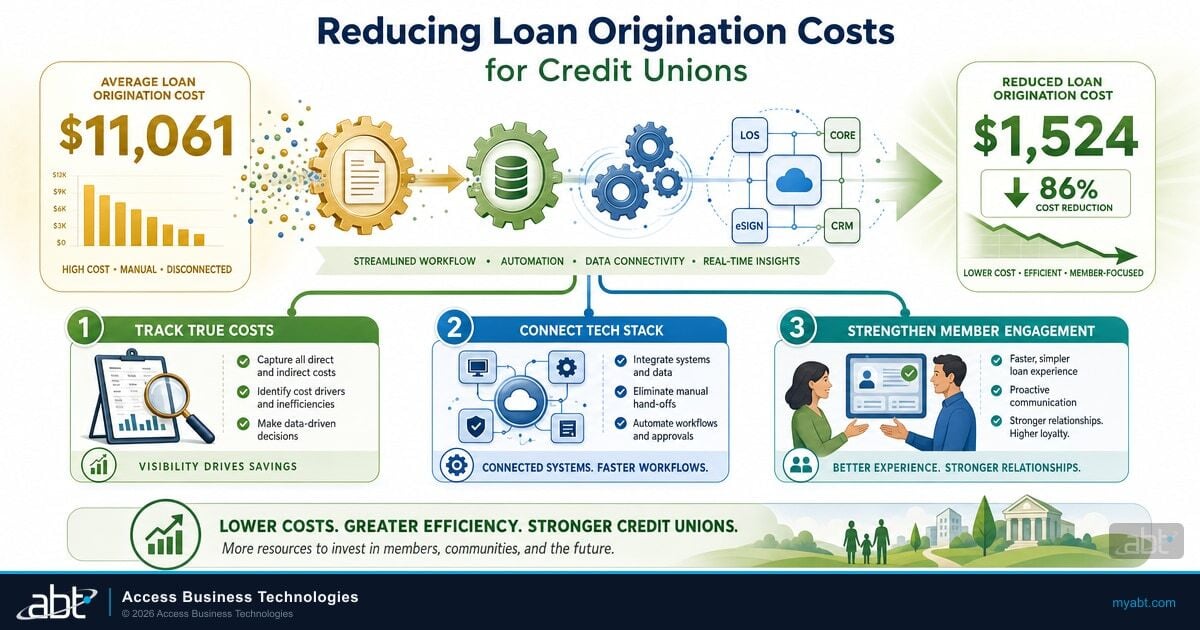

One Nevada's experience offers a template for any institution weighing the cost of integration against the cost of continuing with manual processes. For a deeper dive into the business case for reducing origination costs, this companion analysis lays out the full math.

The math is straightforward. Calculate the hours spent per month on dual data entry, error correction, and post-closing reconciliation. Multiply by fully loaded labor cost. Add the risk cost of wire errors, compliance findings, and delayed member service. That total is the annual cost of not integrating.

Compare it to the cost of MortgageExchange deployment and ongoing managed service fees. For most institutions processing more than a few hundred loans per year, the integration pays for itself within the first year -- and the savings compound as volume grows.

One Nevada's investment in MortgageExchange now delivers returns on every loan, whether it is a first-time homebuyer in Las Vegas or a retiree accessing home equity in Reno. Faster funding, fewer errors, stronger compliance, and a staff that focuses on what credit unions exist to do: serve their members.

ABT serves 750+ financial institutions as a cloud-first MSP and Tier-1 Microsoft CSP. MortgageExchange supports over 40 mortgage technology systems and is managed end-to-end by ABT on Microsoft Azure.

Technical Reference

The following terms are common in credit union and mortgage technology integration environments:

- MortgageExchange: ABT's cloud-managed integration platform that connects loan origination systems, core banking platforms, servicing software, and wire transfer systems through pre-built connectors and configurable business rules. Supports 40+ mortgage technology systems. Hosted on Microsoft Azure.

- Central Integration Layer: An architecture where multiple systems connect to a central middleware platform (MortgageExchange) rather than directly to each other. This reduces the number of integration points from N-squared to N, simplifying maintenance and upgrades.

- Loan Origination System (LOS): Software that processes mortgage applications from intake through closing. Forward mortgage LOS platforms include Encompass, OpenClose, and Calyx Point. Reverse mortgage platforms include QuantumReverse and ReverseVision.

- Core Banking System: The central platform managing member or customer accounts, transactions, and the general ledger. Common credit union cores include Jack Henry Symitar, Fiserv DNA, and Corelation KeyStone.

- HECM (Home Equity Conversion Mortgage): A federally insured reverse mortgage product that allows homeowners aged 62 and older to convert home equity into cash. HECMs are originated through specialized reverse mortgage LOS platforms.

Eliminate dual data entry across your mortgage stack

One Nevada cut re-keying to zero across five systems and two mortgage lines. ABT can map your origination, core, servicing, and wire systems the same way through a managed integration hub on Microsoft Azure.

Frequently Asked Questions

MortgageExchange uses a central integration layer where each system -- the loan origination system, core banking platform, servicing software, and wire transfer system -- connects to MortgageExchange once. The platform handles data extraction, validation, transformation, and routing between all connected systems through a single integration layer rather than individual point-to-point connections.

Dual data entry costs credit unions in direct labor hours, error correction time, delayed loan funding, and compliance risk. Each manual re-entry event introduces potential transcription errors that can trigger regulatory findings during NCUA examinations. For institutions processing hundreds of loans annually, the cumulative labor and risk cost typically exceeds the investment required for MortgageExchange deployment.

Yes. MortgageExchange connects both forward mortgage origination systems like MeridianLink OpenClose and reverse mortgage platforms like QuantumReverse to the same core banking, servicing, and wire transfer systems. MortgageExchange handles the different data formats and business rules for each loan type while routing all data through a unified hub on Microsoft Azure.

MortgageExchange ensures that loan data is identical across the origination system, core banking platform, and servicing software. This consistency is a baseline expectation during NCUA, FFIEC, and state regulatory examinations. MortgageExchange also creates detailed audit trails documenting every data transfer, validation check, and timestamp, satisfying examiner requirements for data integrity documentation.

MortgageExchange's central integration layer connects each financial system to the MortgageExchange platform rather than building direct connections between every pair of systems. For five systems, this requires five connections instead of ten point-to-point integrations. The architecture reduces maintenance complexity, simplifies vendor upgrades, and allows new systems to be added with a single connector.