In This Article

- The Fragmented Technology Stack in Financial Services

- Why Direct-Bill CSP Tenant Management Sits Underneath It All

- Building the Automation Layer

- Custom Interfaces and Managed Application Operations

- Managing 300+ Vendor Relationships

- Compliance Infrastructure That Scales

- Choosing a Managed IT Partner for Financial Services

- Frequently Asked Questions

McKinsey research from 2025 found that administrative burden consumes 70 percent of the average relationship manager's time at financial institutions. That is time not spent with members, borrowers, or commercial clients. It is time spent toggling between systems, entering data, chasing document statuses, and manually reconciling vendor outputs that should connect automatically.

The technology to eliminate most of that burden already lives inside Microsoft 365, Microsoft Azure, and the line-of-business platforms that banks, credit unions, and mortgage companies already pay for. Document AI classifies and extracts data from hundreds of document types with 95 to 99 percent accuracy. Workflow engines route loan files and account applications automatically. Role-specific interfaces give every staff member exactly the data they need without navigating screens built for someone else. The challenge is not finding the tools. It is implementing, integrating, securing, and continuously operating them without disrupting the operations that serve your members and customers today.

That implementation-and-operation gap is where a managed IT partner built specifically for financial institutions becomes the difference between a technology investment that transforms operations and one that adds complexity without measurable return. Access Business Technologies manages Microsoft 365 tenants and hosts Azure environments for more than 750 banks, credit unions, mortgage companies, and securities firms as a Tier-1 Direct-Bill Microsoft Cloud Solution Provider, and runs an operating model on top of that footprint that turns Microsoft 365, Azure, and ABT's custom interface products into the automation layer this article describes.

The Fragmented Technology Stack in Financial Services

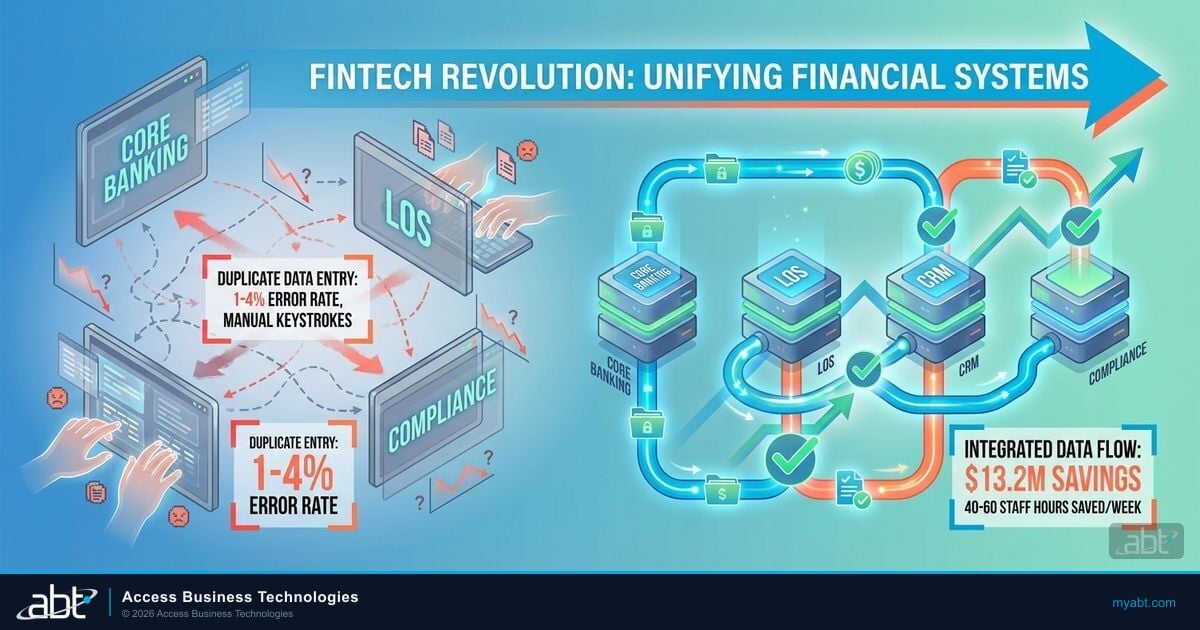

Banks, credit unions, and mortgage companies rarely built their technology stacks from scratch. Most assembled them over decades, adding vendors as needs emerged and patching the gaps between systems with manual workarounds. The result is a fragmented environment where core banking does not speak to the loan origination system, document management operates in isolation, and compliance tracking happens in spreadsheets running alongside systems that should be generating that data automatically.

This fragmentation creates three specific operational problems that compound over time.

Three Ways Fragmented Technology Limits Financial Institution Growth

- Volume ceilings. Manual workflows break under load. When application volume increases 30 percent, staff need 30 percent more hours. Automated workflows absorb volume increases without proportional headcount costs.

- Error compounding. Every manual data transfer introduces risk. Across a pipeline of 500 loan applications, even a 5 percent manual error rate generates 25 files requiring rework, delayed closings, and potential compliance exposure.

- Compliance drift. When compliance requirements are tracked outside the primary workflow, gaps appear. Incomplete audit trails, missed disclosure deadlines, and BSA/AML documentation gaps all trace back to disconnected systems that were never designed to work together.

A managed IT provider built for financial services addresses all three problems at once by managing the Microsoft 365 tenant that anchors identity and collaboration, hosting the Azure environment that runs line-of-business applications, embedding automation into the daily workflow surface, and giving compliance teams the visibility they need across the entire operation. Read more about why generic MSPs fail financial services compliance requirements and what distinguishes providers that actually understand regulated industries.

Why Direct-Bill CSP Tenant Management Sits Underneath It All

Most automation conversations skip the layer that everything else sits on top of: the Microsoft 365 tenant itself. Microsoft owns and operates the M365 service infrastructure. A Tier-1 Direct-Bill Cloud Solution Provider like ABT manages your firm's tenant under delegated administrative permissions granted through the CSP partnership. That delegated-admin relationship is the operational foundation. It is what allows ABT to patch, configure, secure, and report on every Microsoft 365 surface your staff uses every day without your IT team logging into another portal.

A managed Microsoft 365 tenant under a Direct-Bill CSP covers four operational disciplines a generic MSP cannot deliver at the same depth. Patching and update management across Exchange Online, SharePoint Online, OneDrive, Teams, and the Microsoft 365 apps for enterprise so security and feature updates land on a managed cadence rather than a per-user prompt. License rightsizing across Microsoft 365 Business Premium, E3, E5, and the Microsoft 365 Copilot SKUs so the firm pays for what it actually uses, with quarterly true-ups instead of annual surprises. Security baseline configuration across Microsoft Entra ID Conditional Access, Microsoft Defender for Office 365, Microsoft Defender for Endpoint, Microsoft Intune device compliance, and Microsoft Purview Audit so the controls examiners ask about are configured consistently across every user, device, and mailbox. Audit-ready configuration evidence produced on demand for NCUA, OCC, FDIC, FFIEC, and external auditor reviews, sourced directly from the tenant rather than reconstructed from screenshots.

ABT is a Tier-1 Direct-Bill Microsoft Cloud Solution Provider, which means ABT transacts directly with Microsoft, holds dedicated partner support engineers, and is operationally accountable to Microsoft for how customer tenants are configured and run. For a financial institution choosing a managed IT partner, that designation is a fast first-pass filter. It separates partners who resell Microsoft licenses through a distributor from partners Microsoft trusts to operate enterprise-grade tenants at scale. ABT manages Microsoft 365 tenants (Exchange Online, SharePoint, Teams, OneDrive) under delegated admin, and hosts Microsoft Azure environments that run the line-of-business applications your front and back office actually use. M365 Guardian is the operating model ABT layers on top of those Microsoft surfaces, calibrated to the regulatory perimeter community banks, credit unions, and mortgage companies live inside every day.

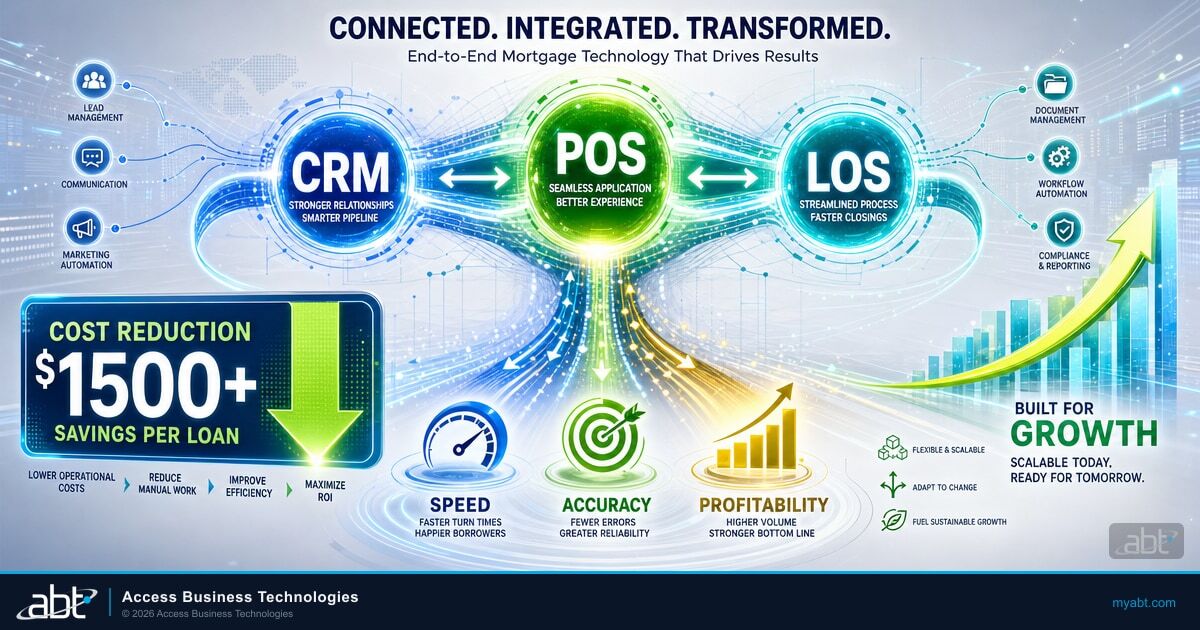

Building the Automation Layer

Automation in financial institution operations covers a wide range of tasks: document classification, data extraction, income verification, identity confirmation, transaction monitoring, disclosure delivery, and member or borrower communications. Each task can be automated individually, but the real value comes from connecting them into workflows where each automated step hands off to the next without human intervention.

Financial-institution-focused managed IT providers approach automation in four connected layers.

Document AI. Modern document processing platforms achieve 95 to 99 percent accuracy across 600 or more document types, compared to 70 to 80 percent for legacy OCR systems (Extend.ai, 2025). A Cognizant case study of a global bank found that generative AI-based document extraction achieved 96 percent accuracy across 20 or more document types, cutting processing time from 30 minutes to 30 seconds (Cognizant, 2024-2025). Documents arriving by email, member portal upload, or mobile capture are classified automatically, key data is extracted and validated, and each document is routed to the correct account or loan file. Staff who previously spent hours sorting and indexing incoming documents spend that time on decisions that require judgment.

Workflow automation. Rules-based workflow engines route applications through the processing pipeline based on loan or account type, complexity, and team capacity. When an underwriter clears a condition, the system notifies the applicant automatically if additional documentation is needed. When all conditions are satisfied, the file advances to the next stage without a human routing it. These engines work across retail and commercial lending, account opening, and member service workflows.

Communication automation. Status updates, document requests, and processing milestones trigger automatically via the member or borrower's preferred channel. Applicants receive accurate progress information without staff manually sending individual updates. Referral partners and commercial clients see real-time status without calling the operations center.

Robotic process automation (RPA). Software robots handle repetitive data-entry tasks that cannot yet be addressed through native API connections. Pulling credit reports, populating form fields across systems, and transferring data between platforms that lack direct integration are common candidates. RPA fills the operational gaps while deeper API integrations are being built and tested.

Custom Interfaces and Managed Application Operations

Loan officers, processors, underwriters, BSA compliance officers, and member-facing staff each interact with the same underlying data in fundamentally different ways. Off-the-shelf platforms force everyone through the same screens, creating friction for every role while optimizing for none. Staff spend time navigating to the data they need instead of acting on it.

Role-specific interface design solves this directly. Each team member sees the data, actions, and workflow views relevant to their job without accessing screens that belong to a different function.

Custom Interface Examples by Financial Institution Role

- Loan officers. Pipeline status, borrower or member communications, pre-qualification results, and referral partner activity. No access to underwriting screens or compliance dashboards that are not part of the sales workflow.

- Loan processors. Document status, condition checklists, file completeness indicators, and outstanding items by loan. Direct access to what is missing and what action is needed.

- Credit underwriters. Risk analysis, income and employment calculations, document verification results, and decision history. The complete picture needed for fast, defensible decisions.

- BSA compliance officers. Transaction monitoring alerts, SAR workflow queues, high-risk account flagging, and audit trail access. Machine learning-assisted alert triage reduces the false-positive rate that consumes compliance staff time.

- Member or customer portals. Account openings, loan applications, document upload, and status tracking from a device-responsive interface that reflects the institution's brand and meets WCAG accessibility standards.

Building the interface is half the work. The other half is operating it in production every day. ABT runs three line-of-business products that sit on top of a managed Microsoft 365 tenant and an ABT-hosted Azure environment. MortgageExchange is the custom interface layer that connects a mortgage company's loan origination system to its core banking platform (Fiserv, Jack Henry, FIS) so data flows in both directions without staff manually transferring records. Mortgage BI is the business intelligence layer that gives executives, branch managers, and originators role-specific views of pipeline performance, broker production, and origination economics. App Pilot is the managed application operations product that wraps the daily lifecycle of MortgageExchange, Mortgage BI, Calyx PointCentral, and other line-of-business applications: deployment, in-app analytics, upgrade testing, and operational SLAs. Custom interface development is one of ABT's foundational practice areas for financial institutions. The pattern observed across hundreds of deployments is consistent: when the interface matches the actual workflow and the application underneath it is operated as a managed service, adoption increases, training time drops, and error rates fall. Read more about how custom interfaces eliminate duplicate data entry across financial institution systems.

Managing 300+ Vendor Relationships

According to Ncontracts' 2025 Third-Party Risk Management Survey, more than half of financial institutions oversee 300 or more technology vendors, and 73 percent of those institutions manage that vendor portfolio with two or fewer dedicated employees. For credit unions under a billion dollars in assets, the typical vendor count falls between 101 and 300 relationships, with 30 percent of those institutions having zero staff fully dedicated to vendor management.

Each of those vendors has its own interface, its own data format, and its own integration requirements. Connecting them into a coherent operational environment is not a technology purchase. It is an ongoing engineering and management practice.

A managed IT partner acts as the integration layer, connecting those vendors into a unified operational environment. Core banking platforms from Fiserv, Jack Henry, or FIS feed data directly into loan origination and account management workflows through ABT's MortgageExchange interface for the mortgage vertical, and through equivalent integration patterns for retail and commercial banking. Identity verification, BSA/AML screening, and credit bureau services trigger automatically at the appropriate workflow stage rather than requiring manual ordering. Document management and e-signature platforms connect to the loan file without staff manually transferring documents between systems. Calyx PointCentral, where mortgage banks use it, runs as a dedicated Azure-hosted instance in an ABT-operated subscription so the application is operated as part of the managed service rather than as a self-managed deployment.

Regulatory Context: Vendor Management Requirements for Financial Institutions

OCC Bulletin 2024-11 (May 2024) requires community banks to manage third-party risk across the full vendor lifecycle, with heightened scrutiny for critical vendors and fintech relationships. The interagency third-party risk guidance (OCC, FDIC, Federal Reserve, 2023) mandates annual financial condition reviews, audit report review, and evaluation of vendor alignment with the institution's strategic goals. NCUA's 2024 supervisory priorities added third-party risk explicitly under information security and cybersecurity, signaling that examiners will evaluate vendor management programs as a core control. Managing 300 or more vendor relationships without a systematic program is increasingly an examination risk.

The practical impact of vendor integration extends beyond efficiency. When systems share data automatically, audit trails are complete, compliance records are accurate, and the institution can demonstrate to examiners that controls work as designed. For community banks and credit unions navigating OCC, FDIC, and NCUA examinations, a well-integrated vendor environment is a compliance asset, not just an operational convenience.

Compliance Infrastructure That Scales

Compliance is not a one-time project. BSA/AML requirements evolve as FinCEN issues new guidance. NCUA and FDIC examination priorities shift annually. State-level privacy requirements add to the federal floor. A compliance infrastructure that works for your institution today needs to adapt to the requirements that come into force next year.

Managed IT providers build compliance into the technology stack rather than adding it as a separate process layer on top of existing workflows. For a Microsoft 365 tenant operated by a Tier-1 Direct-Bill CSP, that work is concentrated in five Microsoft product surfaces. Microsoft Purview Audit produces the tamper-evident time-stamped audit trail across Exchange Online, SharePoint, OneDrive, Teams, and Microsoft Entra ID. Microsoft Purview Information Protection and DLP classify and protect customer NPI, account records, and loan documentation. Microsoft Defender for Office 365 and Microsoft Defender for Endpoint produce the incident detection and response evidence that GLBA, the FTC Safeguards Rule, and amended SEC Regulation S-P require. Microsoft Sentinel aggregates the signals from those Defender surfaces, Entra ID, Intune, and the line-of-business platforms into a single incident timeline. Microsoft Entra ID Conditional Access enforces the MFA and least-privilege expectations examiners look for under FFIEC IT Handbook guidance. ABT manages the configuration of every one of those Microsoft surfaces inside the M365 Guardian operating model so the firm's compliance team works with evidence rather than reconstructing it from screenshots.

TL;DR

- Manual BSA/AML alert queues generate 85 to 95 percent false positive rates under rule-based systems. Machine learning reduces false positives to 50 to 60 percent, roughly doubling analyst productivity (Gartner 2025 Financial Crime Operations Survey).

- Financial institutions deploying intelligent automation report 30 to 40 percent productivity gains in targeted operational areas (McKinsey, 2024-2025).

- OCC Bulletin 2025-37 updated BSA/AML examination procedures. Institutions with well-documented automated controls receive appropriately tailored examination approaches.

Specific compliance capabilities a financial-institution-focused managed IT provider should deliver include:

- Automated disclosure management. Loan estimates and closing disclosures generated and delivered within regulatory timing requirements, with receipt tracking and tolerance monitoring embedded in the workflow.

- Regulatory change management. When GLBA, the FTC Safeguards Rule, or state-level requirements change, the managed provider updates the compliance configuration. The operations team acts on decisions, not on interpreting regulatory amendments.

- Audit-ready documentation. Every workflow action is logged automatically. Every decision has a traceable record. When OCC, FDIC, or NCUA examiners arrive, the evidence is organized rather than reconstructed from email threads and shared drives.

- Scalable architecture. Compliance rules run automatically on every application and transaction, regardless of volume. The system handles 200 or 2,000 loan applications per month without adding compliance staff proportionally.

For security compliance specifically, interface security best practices for financial institution platforms covers the technical controls that should be built into every custom interface and portal used by staff and members.

Choosing a Managed IT Partner for Financial Services

Not every managed IT provider is equipped to serve a financial institution. A generalist technology partner can manage workstations, support email, and maintain basic infrastructure. But transforming a fragmented operational environment, managing a Microsoft 365 tenant under delegated admin, hosting an Azure environment that runs your line-of-business applications, integrating core banking vendors, building custom staff interfaces, and maintaining compliance infrastructure requires industry-specific knowledge that most providers do not have.

Key criteria for evaluating a managed IT partner in financial services:

- Financial institution client base. Does the provider work specifically with banks, credit unions, and mortgage companies, or do financial institutions represent a small portion of a broader client mix? Industry-specific experience translates directly to faster deployment, fewer integration surprises, and staff who understand regulatory language.

- Tier-1 Direct-Bill CSP status. A Direct-Bill CSP transacts with Microsoft directly, holds dedicated partner support engineers, and is operationally accountable to Microsoft. That designation is a fast first-pass filter that separates resellers from partners Microsoft trusts to operate enterprise tenants at scale.

- Integration depth. Can the provider connect your core banking platform, loan origination system, document management system, and BSA/AML vendor through certified APIs, or do they rely on manual bridges? Ask for specific references to the integrations your institution requires.

- Compliance fluency. Does the provider understand NCUA, OCC, FDIC, and FFIEC requirements as operational realities, not just regulatory names? Compliance mistakes are expensive. Providers who understand the exam environment design systems that hold up under scrutiny.

- Security posture and certifications. Financial institution data is regulated data. The provider's infrastructure must meet SOC 2 Type II, GLBA, and applicable investor or secondary market requirements. Ask for current certifications and the scope of those certifications.

- Scalability history. Has the provider supported institutions through volume spikes, mergers, or product launches without proportional cost increases? Ask for specific examples of institutions they supported through significant operational changes.

Community banks and credit unions also benefit from working with a provider that holds direct Microsoft licensing relationships. A Tier-1 Direct-Bill CSP negotiates licensing directly with Microsoft and can configure Microsoft 365, Azure, and Microsoft 365 Copilot deployments within the same managed service contract, eliminating an additional vendor relationship. Learn more about why community banks benefit from a Tier-1 CSP over a generic managed service provider.

Your Operations Should Run on More Than Manual Effort

ABT manages Microsoft 365 tenants and hosts Azure environments for more than 750 banks, credit unions, mortgage companies, and securities firms as a Tier-1 Direct-Bill Microsoft Cloud Solution Provider. The M365 Guardian operating model plus MortgageExchange, Mortgage BI, and App Pilot turn that Microsoft footprint into the automation layer this article describes. A 30-minute conversation maps your current tenant, Azure environment, and line-of-business stack against where automation actually pays off.

Frequently Asked Questions

A financial-institution-focused managed IT provider builds connected automation across document classification, data extraction, income and identity verification, workflow routing, disclosure delivery, and member communications. The work usually sits on top of a managed Microsoft 365 tenant, an ABT-hosted Azure environment, and a set of line-of-business interfaces (MortgageExchange for mortgage banks, equivalent integration patterns for retail and commercial banking) operated under the M365 Guardian operating model. AI-powered document platforms classify and extract data from hundreds of document types with 95 to 99 percent accuracy, and workflow engines route applications automatically based on type, complexity, and team capacity. The goal is connecting these systems into a continuous workflow rather than automating each task in isolation.

A general managed service provider supports hardware, email, and basic infrastructure. A financial institution IT partner manages the Microsoft 365 tenant under delegated administrative permissions, hosts the Azure environment that runs line-of-business applications, understands core banking platforms, loan origination systems, BSA/AML requirements, NCUA and OCC examination priorities, and the compliance controls required by GLBA, the FTC Safeguards Rule, and applicable state requirements. They build custom interfaces for specific staff roles, integrate vendor ecosystems through direct API connections, and embed compliance documentation into the operational workflow rather than treating it as a separate process. Tier-1 Direct-Bill CSP status is a fast first-pass filter that separates resellers from partners Microsoft trusts to operate enterprise tenants at scale.

Microsoft owns and operates the Microsoft 365 service infrastructure. A Tier-1 Direct-Bill Cloud Solution Provider like ABT manages the customer tenant under delegated administrative permissions granted through the CSP partnership. That covers four operational disciplines a generic MSP cannot match at the same depth. First, patching and update management across Exchange Online, SharePoint, OneDrive, Teams, and the Microsoft 365 apps for enterprise on a managed cadence. Second, license rightsizing across Microsoft 365 Business Premium, E3, E5, and Microsoft 365 Copilot SKUs with quarterly true-ups rather than annual surprises. Third, security baseline configuration across Microsoft Entra ID Conditional Access, Microsoft Defender for Office 365, Microsoft Defender for Endpoint, Microsoft Intune device compliance, and Microsoft Purview Audit so the controls examiners ask about are configured consistently. Fourth, audit-ready configuration evidence produced on demand for NCUA, OCC, FDIC, FFIEC, and external auditor reviews, sourced directly from the tenant rather than reconstructed from screenshots.

According to the Ncontracts 2025 Third-Party Risk Management Survey, more than half of financial institutions oversee 300 or more technology vendors. Credit unions under one billion dollars in assets typically manage between 101 and 300 vendor relationships. Seventy-three percent of financial institutions manage this vendor portfolio with two or fewer dedicated employees. A managed IT partner that functions as an integration layer connects those vendors into a unified operational environment, reducing the manual coordination burden on internal staff. For mortgage banks, that integration layer is usually MortgageExchange connecting the loan origination system to the core banking platform. For all financial institutions, the layer underneath is the managed Microsoft 365 tenant and the ABT-hosted Azure environment that the line-of-business applications run in.

A financial institution managed IT provider should deliver automated disclosure management within TRID and other applicable regulatory timing requirements, regulatory change management that updates compliance configurations when GLBA, the FTC Safeguards Rule, or state requirements change, and complete audit trail automation that logs every workflow action and decision. Inside a managed Microsoft 365 tenant, the controls concentrate in Microsoft Purview Audit, Microsoft Purview Information Protection and DLP, Microsoft Defender for Office 365, Microsoft Defender for Endpoint, Microsoft Sentinel, and Microsoft Entra ID Conditional Access. The infrastructure should meet OCC, FDIC, NCUA, and FFIEC examination standards and scale to handle volume growth without requiring proportional increases in compliance staff. ABT manages the configuration of each of those Microsoft surfaces inside the M365 Guardian operating model.

Custom interfaces give each staff role access to the specific data, actions, and workflow views they need without requiring them to navigate screens built for different functions. Loan officers see pipeline and borrower status. Processors see document and condition checklists. BSA compliance officers see transaction monitoring queues and audit trails. ABT's MortgageExchange custom interface and Mortgage BI dashboards are operated under the App Pilot managed application operations product, which means deployment, in-app analytics, upgrade testing, and operational SLAs are part of the managed service rather than the firm's responsibility. When the interface matches the actual workflow and the application underneath is operated as a managed service, adoption rates increase, training time decreases, and data entry errors fall because staff are working in a system designed for their specific role and run by a partner who owns the application's uptime.