In This Article

- What Automated Decisioning Systems Do for Financial Institutions

- How Automated Decisioning Technology Works: Three Stages

- The Data Pipeline Problem: Where MortgageExchange Fits In

- Major Platform Updates Reshaping Decisioning in 2026

- Speed and Consistency That Manual Review Cannot Match

- Monitoring Decision Outcomes with Mortgage BI and M365 Copilot

- The Compliance Advantage of Automated Decisioning

- Securing the Decisioning Environment: the M365 Guardian Operating Model

- Where AI-Powered Decisioning Is Heading

- Getting Your Implementation Right

- Frequently Asked Questions

Dark Matter Technologies became the first platform provider to support AI agents inside its decisioning engine using Model Context Protocol in February 2026. Business teams can now build and deploy AI agents that interact with core systems through a secure, auditable gateway. That follows Fannie Mae's partnership with Palantir to detect fraud using AI and the continued rollout of expanded risk assessment capabilities across the industry.

The pattern is clear across credit unions, banks, and mortgage companies: automated decisioning systems are absorbing capabilities that were separate products 18 months ago. These platforms now handle fraud detection, non-traditional income analysis, and condition clearing in the same processing pass. Financial fraud risk rose 8.2% year-over-year in Q3 2025 according to Cotality. AI-driven decisioning is one of the few tools that can match that rising risk with equally fast detection.

If your institution still routes standard applications through manual review, you are spending staff hours on work that machines handle with better consistency. The harder question is not whether to automate. It is whether your data pipeline, your monitoring layer, and your underlying Microsoft 365 environment are ready to support automated decisioning at scale. This article walks through how automated decisioning works, what changed in 2025 and 2026, where ABT's MortgageExchange interface and Mortgage BI dashboards fit into the picture, and how the M365 Guardian operating model keeps the whole pipeline audit-ready.

What Automated Decisioning Systems Do for Financial Institutions

An automated decisioning system evaluates applications using algorithms and data analytics instead of manual human review. It pulls together a customer's credit history, income, employment, debt obligations, and relevant financial data, then runs it all against institutional guidelines to produce an approve, refer, or deny recommendation.

In the mortgage space, the two dominant platforms are Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA), which together process millions of applications annually with accuracy rates around 95% for standard products. Companies like Gateless now report 70-75% auto-clearing rates on credit, income, and asset conditions, with a target of 85% by late 2026.

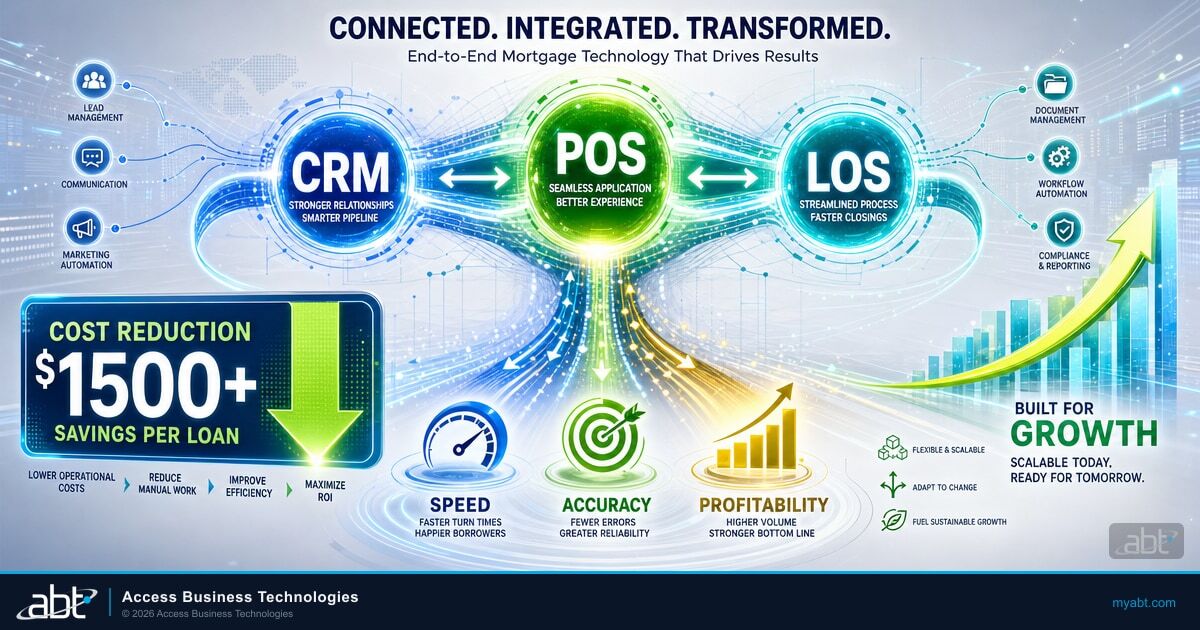

For credit unions and banks, automated decisioning extends beyond mortgage lending into consumer loans, commercial credit, and account risk screening. The same principles apply: clean data in, consistent decisions out, full audit trails for examiners. The institutions getting real results from automation share a common architecture. Their loan origination system, their core banking platform, and their decisioning engine talk to each other through a managed interface layer that ABT calls MortgageExchange. We will come back to that in the data pipeline section.

- AUS

- Automated Underwriting System. Evaluates loan applications against lending guidelines using algorithms and data analytics to produce approve, refer, or deny recommendations.

- DU

- Desktop Underwriter. Fannie Mae's automated underwriting platform for conforming mortgage loans.

- LPA

- Loan Product Advisor. Freddie Mac's automated underwriting platform with proprietary risk models.

- MCP

- Model Context Protocol. A secure gateway standard for AI agents to interact with core business systems.

- LOS

- Loan Origination System. The platform that captures applications, manages documents, and orchestrates the loan workflow before it reaches the decisioning engine.

Automated decisioning does not replace experienced analysts. It handles routine evaluations so your team focuses on complex cases, exception handling, and customer relationships. Institutions that implement it well see their analysts shift from data entry to decision-making.

How Automated Decisioning Technology Works: Three Stages

Automated decisioning operates in three stages: data collection, enrichment, and decisioning. Understanding each stage helps you evaluate platforms and diagnose bottlenecks in your own workflow.

Data Collection

Customer information enters the system through APIs, OCR technology for scanned documents, or RPA wrappers that extract data from existing forms. The quality of this intake determines everything downstream. Institutions using digital verification at the front end see fewer exceptions and faster processing.

Data Enrichment

The system pulls third-party data from credit bureaus, employment verification databases, banking institutions, and relevant databases. DU Version 12.0 expanded this enrichment layer to include cashflow assessment for all borrowers and broader use of rent payment history data. Fannie Mae reports that loans with at least one digital validation component are 33% less likely to produce defects.

Decisioning

Algorithms evaluate risk across multiple dimensions simultaneously: credit history patterns, income stability, debt composition, and relevant characteristics. Each factor receives weighting based on statistical models trained on millions of outcomes. The system produces a recommendation with clear explanations, specific conditions, and documentation requirements.

Modern platforms go beyond approve or deny. They recommend specific products, flag compliance issues, and generate the audit trail that regulators require.

The Data Pipeline Problem: Where MortgageExchange Fits In

A decisioning engine is only as good as the data flowing into it. The credit unions, banks, and mortgage companies that get the most from DU, LPA, and the newer AI-augmented platforms have one thing in common. They have already solved the data pipeline problem. They have a managed interface layer that pulls borrower data, employment verification, account history, and product configurations out of their loan origination system and their core banking platform, normalizes it, and feeds it to the decisioning engine in the form that the engine expects.

ABT operates that interface layer for hundreds of financial institutions under the product name MortgageExchange. It is the custom integration that connects an institution's loan origination system, such as Encompass, Calyx, or Empower, to the core banking platform, such as Fiserv DNA, Symitar Episys, or Jack Henry's Synapsys, and on to the decisioning engine. Without that interface, an analyst is rekeying borrower data from one system into another. With it, the borrower's application arrives at the decisioning engine pre-populated, validated against the core, and tagged with the right product and program codes. For an introduction to how that integration layer is built, see our overview of mortgage data integration for financial institutions and our deeper article on tracking your mortgage pipeline across integrated systems.

The data lake that MortgageExchange populates is also where Mortgage BI dashboards read from and where M365 Copilot agents can be grounded for compliance-aware analysis. Treating decisioning as a standalone deployment misses the larger picture. The pipeline is the product.

Major Platform Updates Reshaping Decisioning in 2026

The major platforms have undergone their most significant updates in years. If you are operating on assumptions from 2023 or earlier, your decisioning criteria may be out of sync with what current systems support.

FICO floor removed. Expanded cashflow assessment. Revised first-time buyer evaluation. Student loan recalibration.

AI-powered fraud detection scanning millions of datasets for patterns that rule-based systems miss.

Revised rental income calculations, updated Income Calculator, alignment with 2026 FHA and VA loan limits.

First platform to support Model Context Protocol for secure AI agent interactions with core lending systems.

ADU income eligibility, HomeStyle Refresh capabilities, expanded manufactured housing options.

These updates matter for all financial institutions, not just mortgage lenders. The risk assessment models, data enrichment capabilities, and AI governance patterns established by DU and LPA are filtering into credit union and bank decisioning platforms across the industry.

Speed and Consistency That Manual Review Cannot Match

Speed is the obvious advantage. Consistency is the more important one.

When a manual reviewer examines ten files in a day, decision quality varies based on experience, fatigue, and individual judgment. When an automated system reviews those same ten files, every application gets evaluated against identical criteria. That consistency reduces fair lending risk, produces more predictable portfolio performance, and gives your compliance team reliable audit documentation.

Scenario: Manual Review Inconsistency

A credit union processes consumer loan applications manually. Two analysts review similar applications on the same day. One approves a borderline case. The other denies a nearly identical application.

Consequence

The inconsistency creates fair lending exposure under ECOA. During examination, the regulator asks why two comparable applicants received different outcomes. Manual review provides no data-driven answer.

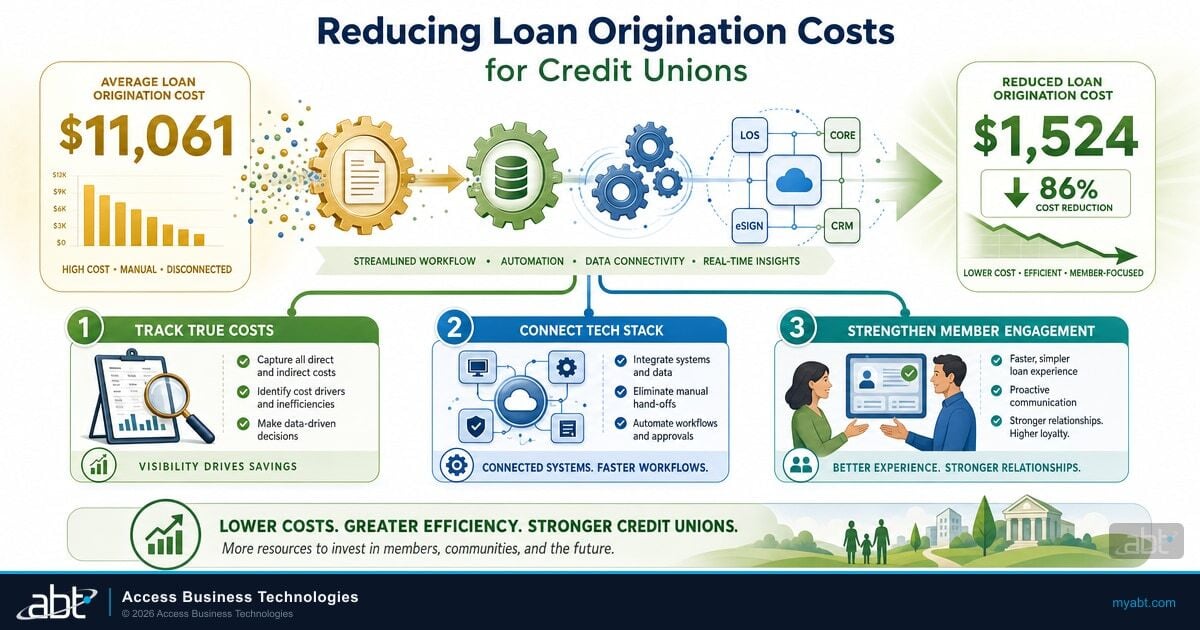

The speed advantage is still significant. Rocket Mortgage processes 1.5 million documents monthly with AI-powered systems that auto-identify 70% of them, saving over 5,000 staff hours per month. For mid-market credit unions, banks, and mortgage companies, automated decisioning creates capacity without adding headcount.

Monitoring Decision Outcomes with Mortgage BI and M365 Copilot

Automating the decision is one job. Knowing whether the decisions are working is a separate job. Institutions that treat the decisioning engine as a black box end up with a portfolio they cannot explain to examiners and a fair lending posture they cannot defend. The institutions that pass clean exams have a monitoring layer that watches decision outcomes by product, by branch, by loan officer, and by protected class continuously, not at quarter end.

That monitoring layer is where two more ABT products come in. Mortgage BI is the business intelligence platform that reads from the same MortgageExchange data lake and produces the dashboards a compliance officer, a chief lending officer, or a board IT committee can act on. Approval rates by branch. Denial reasons by product. Time-to-decision by loan officer. Disparate-impact ratios by ECOA-protected category. Pull-through rates from approval to closing. Decision overrides by analyst. The dashboards refresh as the decisioning engine produces decisions, so the picture is current rather than 60 days stale.

The next layer is Microsoft 365 Copilot. With Copilot Business or Copilot in M365 E5, an analyst can ask Copilot in plain English what changed week-over-week in the denial mix, why a particular product line saw a drop in pull-through, or which branch has the highest exception rate this quarter. Copilot reads the BI surface and returns a grounded answer with citations back to the source dashboards. That turns the BI layer from a tool that only a power user knows how to drive into a tool that the whole lending and compliance team uses. ABT manages the Microsoft 365 tenant that Copilot runs in, configures the data boundaries, and keeps Copilot grounded to the institution's own data rather than to the public internet. For pricing context on the SMB-first Copilot tiers, see our Microsoft 365 Copilot pricing buyer's guide.

Every application gets the same evaluation criteria. That removes the inconsistency that triggers ECOA scrutiny and gives examiners data-driven answers for every lending decision.

The Compliance Advantage of Automated Decisioning

Financial services operates under TILA, RESPA, ECOA, HMDA, BSA/AML, and state-level regulations. Manual processing creates compliance risk every time a decision lacks clear documentation or deviates from published criteria.

Automated platforms generate machine-readable decision explanations for every application. Each decision includes the specific factors that influenced the outcome, the data sources consulted, and the criteria applied. This creates the audit trail that examiners expect.

Fair lending compliance is where automated decisioning provides its strongest regulatory advantage. When regulators ask why applicant A was denied while applicant B was approved, the system provides an answer tied to the risk model rather than individual discretion. AI-driven systems reduced fraud cases by 20% in 2025 by catching anomalies in documentation, data, and application patterns that manual reviewers miss.

Securing the Decisioning Environment: the M365 Guardian Operating Model

An automated decisioning pipeline is one of the most sensitive data flows a financial institution operates. It carries borrower personally identifiable information, credit bureau data, employment verification, account balances, and the institution's own pricing and risk models. The pipeline lives in Microsoft 365, Microsoft Azure, third-party LOS and core platforms, and the decisioning engine itself. Every one of those surfaces is a potential exposure point. Examiners under amended Regulation S-P, NCUA part 748, and FFIEC IT examination guidance are increasingly explicit that they expect to see consistent, documented technical controls across every system in the data flow.

ABT runs that security and configuration layer under an operating model branded M365 Guardian. ABT manages the Microsoft 365 tenant that hosts the workforce identity, the device fleet, the SharePoint and OneDrive document libraries, and the Teams collaboration channels that the lending operation uses. ABT hosts the Azure environments that run MortgageExchange and the BI data lake. Guardian layers Microsoft Entra ID Conditional Access, Microsoft Defender, Microsoft Purview retention and data loss prevention, and Microsoft Intune device compliance over that footprint. The Microsoft 365 Lighthouse multi-tenant management plane gives ABT a single console view across every tenant in the institution's footprint, so the same baseline is applied to every branch and every affiliated entity.

The institution continues to own the loan, the customer, and the regulatory relationship. ABT operates the technology underneath in a configuration that examiners recognize. The decisioning engine, the BI dashboards, the Copilot grounding, and the MortgageExchange data lake all run inside that Guardian-managed envelope.

Where AI-Powered Decisioning Is Heading

The next generation of automated decisioning goes beyond rule-based automation into predictive intelligence. Several capabilities are already in deployment across credit unions, banks, and mortgage companies.

- Predictive default modeling: AI systems analyze 10,000+ data points per application compared to the 50-100 that traditional models consider. This depth enables default risk prediction with 92% accuracy versus 87% for human reviewers.

- AI agents inside core platforms: Dark Matter Technologies launched secure AI agent support using Model Context Protocol. Business teams build agents that interact with core systems through an auditable gateway, keeping AI activity compliant while reducing manual processing tasks.

- Non-traditional product automation: A&D Mortgage launched the first automated decision system for non-QM products. Self-employed borrowers, investors, and foreign nationals now get real-time decisions. This brings automated efficiency to segments that relied entirely on manual review.

- Autonomous processing: Gateless reports that its best-performing clients process 18-20% of applications through initial decisions without any human touch, with a target of 85% auto-clearing by late 2026.

Getting Your Implementation Right

Technology alone does not deliver results. The institutions that get the most from automated decisioning share three characteristics.

Key Takeaway

Clean data at intake, redesigned analyst workflows, and continuous model governance separate institutions that get real value from automated decisioning from those that just added another system to maintain. The interface layer that feeds the decisioning engine, the BI layer that monitors its outputs, and the Microsoft 365 environment that hosts the whole pipeline matter as much as the engine itself.

Clean data at intake. Automated systems are only as good as the data they receive. Institutions that digitize document collection and use API-based verification see faster processing, fewer conditions, and lower defect rates. Fannie Mae data shows applications with digital validation are significantly less likely to produce post-closing defects. The interface layer that connects the LOS to the core, such as ABT's MortgageExchange, is where that intake quality lives or dies.

Analyst workflow redesign. Dropping automation into an existing manual workflow creates bottlenecks. Successful implementations reassign analysts to exception handling, complex case review, and customer relationships. The goal is higher-value work, not fewer people. A BI dashboard that surfaces the exceptions worth working on, and a Copilot the analyst can ask plain-English questions of, makes the workflow redesign stick.

Continuous model governance. Automated models require oversight. Institutions need to track decision accuracy, monitor for unintended bias, and keep systems aligned with current regulatory guidance. This matters more as platforms release updates that change how risk factors are weighted. The Guardian operating model produces the configuration evidence, the Purview audit log, and the Sentinel incident timeline that examiners ask for when they audit the model governance.

Talk to ABT About Your Decisioning Pipeline

ABT operates MortgageExchange, Mortgage BI, and the M365 Guardian operating model for more than 750 banks, credit unions, and mortgage companies. A 30-minute conversation maps your current decisioning pipeline, surfaces the interface and monitoring gaps that slow down both speed and audit readiness, and outlines what an ABT-operated environment would cover. No commitment, no quote, no obligation.

Frequently Asked Questions

An automated decisioning system evaluates applications using algorithms and data analytics to assess creditworthiness, income stability, debt levels, and relevant characteristics. For mortgage lending, the two primary platforms are Fannie Mae's Desktop Underwriter and Freddie Mac's Loan Product Advisor. Credit unions and banks use similar platforms for consumer lending, commercial credit, and risk screening. These systems process applications against institutional guidelines and produce recommendations within minutes. The quality of the recommendation depends heavily on the data pipeline feeding the engine, which is where interface layers such as ABT's MortgageExchange become decisive.

MortgageExchange is ABT's custom interface layer that connects a financial institution's loan origination system, such as Encompass, Calyx, or Empower, to its core banking platform, such as Fiserv DNA, Symitar Episys, or Jack Henry's Synapsys, and on to the automated decisioning engine. The interface pulls borrower data, employment verification, account history, and product configurations out of the source systems, normalizes the data, and feeds the decisioning engine in the form the engine expects. Without that interface, analysts rekey borrower data between systems and the decisioning engine receives lower-quality inputs. With it, decisions are faster and the audit trail is cleaner. MortgageExchange also populates the data lake that Mortgage BI and Microsoft 365 Copilot read from.

Automated systems handle routine evaluations but do not replace experienced analysts. Top-performing systems currently auto-clear 70-75% of standard conditions, with targets of 85% by late 2026. Complex scenarios, exception cases, and non-standard situations still require human judgment. Successful institutions use automation to redirect analyst expertise toward high-value work including complex case analysis and quality control oversight, often supported by Mortgage BI dashboards and Microsoft 365 Copilot grounded to the institution's own data.

Automated decisioning applies identical evaluation criteria to every application, removing human judgment variability that creates ECOA compliance risk. Each decision generates a documented audit trail showing which factors influenced the outcome and which data sources were consulted. This consistency reduces disparate treatment claims and gives examiners clear, data-driven explanations for every decision. Continuous monitoring through a BI layer such as Mortgage BI surfaces disparate-impact ratios by protected class so the institution can act on patterns before an examiner does.

Microsoft 365 Copilot, in its Copilot Business or Copilot in M365 E5 form, sits on top of the Mortgage BI data and the institution's own SharePoint, OneDrive, Teams, and Outlook content. Analysts and compliance officers can ask Copilot in plain English what changed in the decision mix, why a product line saw a drop in pull-through, or which branch has the highest exception rate. Copilot returns a grounded answer with citations back to the source dashboards and documents. The value depends on the data boundary: ABT manages the M365 tenant so Copilot is grounded to the institution's own data and the workforce identity controls, Conditional Access policies, and Purview data protections that examiners expect to see.

AI-powered fraud detection identifies patterns that rule-based systems miss by analyzing behavior across multiple institutions, geographies, and time periods. Fannie Mae partnered with Palantir in May 2025 to launch an AI Crime Detection Unit scanning millions of datasets. AI systems adapt to new fraud tactics continuously without requiring manual rule updates. The Mortgage Bankers Association reports AI reduced fraud cases by 20% in 2025. The institutions that get the most from AI fraud detection feed it from a clean integration layer and watch the outputs through a BI dashboard that surfaces anomalies in real time.

Three factors determine success: clean data at intake through digitized document collection and API-based verification, workflow redesign that reassigns analysts to exception handling and complex cases, and continuous model governance that tracks decision accuracy and monitors for unintended bias. Institutions that skip any of these steps see bottlenecks and compliance gaps that undermine the system's value. The interface layer that handles intake, the BI layer that handles monitoring, and the Microsoft 365 environment that hosts the whole pipeline all need to be operating at the same standard. The M365 Guardian operating model is how ABT keeps that standard consistent across the institution's footprint.