It's 8:15 a.m. in mortgage operations at Thrivent Federal Credit Union. A loan officer finishes a closing in Mortgage Cadence LFC. Across the hall, someone in operations starts prepping the Dovenmuehle (DMI) boarding package. A teammate updates the member profile in Fiserv DNA. Account services checks MeridianLink Opening for the new membership the borrower requested.

Four systems. Four people. The same fifteen data fields, typed four times.

If a single digit lands wrong, the afternoon disappears into reconciliation calls, re-run files, and apology emails. This isn't a system failure. It's Tuesday.

In This Article

- Four Good Systems, Zero Shared Data

- Why Point-to-Point Bridges Break at Scale

- How MortgageExchange Orchestrates the Data Flow

- The Real Cost of Swivel-Chair Integration

- What MortgageExchange Means for Compliance and Audit Readiness

- Outcomes at Thrivent FCU

- From Thrivent FCU to Thrivent Bank

- How ABT and MortgageExchange Serve Credit Unions

- Frequently Asked Questions

Four Good Systems, Zero Shared Data

Thrivent FCU operated a best-of-breed technology stack that most credit unions would envy. Mortgage Cadence LFC handled loan origination. Fiserv DNA ran the core banking platform. MeridianLink Opening managed account origination. Dovenmuehle Mortgage (DMI) serviced loans post-closing. Each platform was strong on its own. None of them shared data automatically.

The result was a pattern credit union operations teams know too well: swivel-chair integration. Staff pivoted between screens, re-keying the same borrower details because the systems couldn't pass information themselves. Jack Henry's 2025 Strategy Benchmark reported that 31 percent of credit unions whose tech plans fell short cited integration challenges as a primary cause, alongside 53 percent who pointed to insufficient vendor support and 39 percent who saw longer-than-expected implementation timelines. The pattern is industry-wide, and it lands hardest on credit union operations teams running multi-vendor stacks.

Thrivent's leadership drew a clear line: data should be captured once and trusted everywhere. That meant connecting the LOS to three critical downstream platforms so information could move on its own, validated and consistent, without employees acting as human middleware.

Why Point-to-Point Bridges Break at Scale

The obvious first instinct is to build direct connections between each pair of systems. LOS to core. LOS to servicing. Core to account opening. But point-to-point bridges create a combinatorial problem. Four systems produce six possible connections, each requiring its own mapping, its own error handling, its own maintenance schedule.

When a vendor pushes an API update, every bridge touching that system breaks. When a fifth platform enters the mix, the connection count jumps to ten. Credit unions that go down this road end up with spaghetti architecture that only one or two people understand. Those people become the most dangerous single points of failure in the organization.

Why This Matters for Credit Union Operations Leaders

Cornerstone Advisors' What's Going On in Banking 2026 survey of 416 senior executives at community banks and credit unions found that more than 80 percent plan to increase technology spending in 2026, with persistent execution gaps between strategy and tech deployments cited as the top friction. The danger isn't underspending. The danger is buying more platforms without solving the connective tissue that makes them work together.

Thrivent chose a different approach: MortgageExchange from Access Business Technologies. Rather than commissioning one-off scripts or brittle bridges, the credit union deployed a cloud-managed, rules-based integration platform built specifically to connect LOS, core banking, account opening, and servicing systems at scale. Credit unions running similar integration patterns can see this approach applied in Bay Federal Credit Union's post-closing automation work and in CFCU Community Credit Union's mortgage data reconciliation rebuild.

How MortgageExchange Orchestrates the Data Flow

MortgageExchange operates on event-driven rules. When a loan reaches a milestone in Mortgage Cadence LFC (approved, closed, funded), the platform automatically pushes the right data to the right destination:

- Core banking updates post to Fiserv DNA so member records stay current without duplicate typing.

- Validated loan packages flow to DMI for servicing setup. No more CSV file gymnastics or manual boarding forms.

- Account-opening requests route to MeridianLink Opening with exactly the fields needed when a new membership or account change is part of the lending journey.

Under the hood, MortgageExchange's mapping and validation engine enforces data integrity before anything moves. If a required field is missing, if a value falls outside policy parameters, the system flags it in real time. The error surfaces before it becomes someone's afternoon crisis, not three days later during a reconciliation audit.

Because the integration runs as a cloud-managed service, ABT maintains the connectors. When Fiserv pushes a DNA update or DMI changes their boarding file spec, MortgageExchange adapts without Thrivent's team writing a single line of code. The integration runs continuously in the background: reliable, observable, and boring in the best possible way.

The Real Cost of Swivel-Chair Integration

Every closed loan at Thrivent triggered a cascade of manual keystrokes before MortgageExchange. Copy the borrower info. Re-enter loan terms. Double-check escrow fields. Regenerate a boarding file. Every step introduced a typo risk. Every handoff introduced lag. And while the team had mastered the routine, the routine kept them away from members.

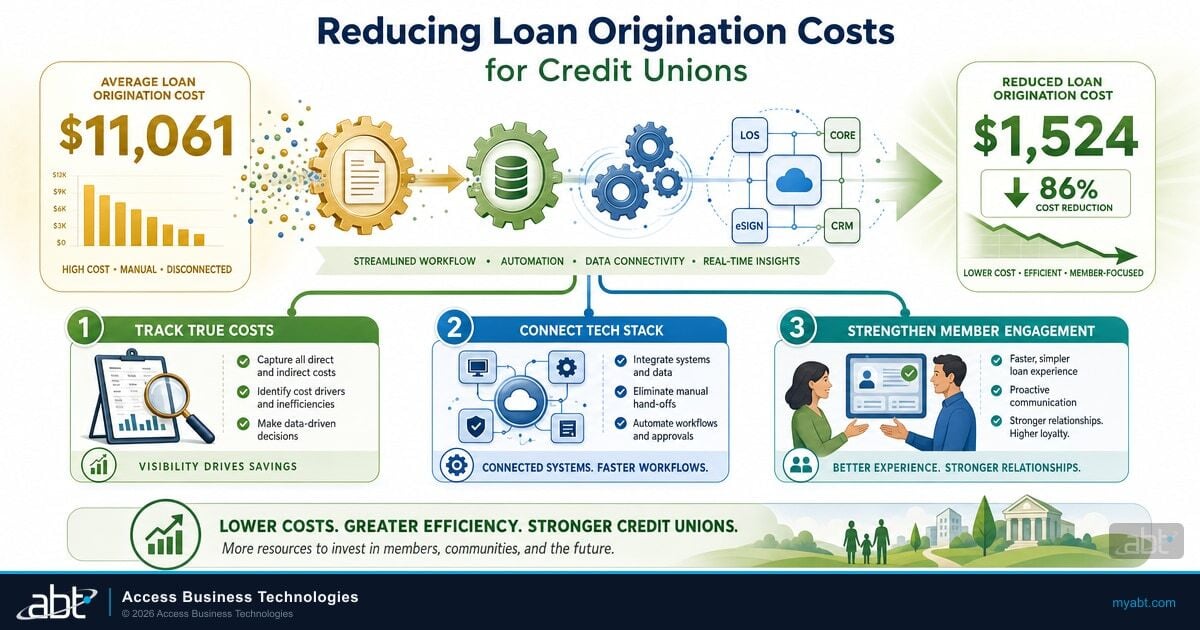

The math is unforgiving when measured against industry benchmarks. The Mortgage Bankers Association's Q3 2025 report pegged average production cost at $11,109 per loan, while Freddie Mac's 2025 update to its Cost to Originate study placed retail mortgage production around $11,800 per loan and credited digital capabilities like Loan Product Advisor with savings of up to $1,700 per loan when applied at scale. Even a conservative 5 percent reduction from data-integration automation translates to roughly $555 per loan. For a credit union closing 200 loans monthly, that's approximately $111,000 per month in addressable cost reduction tied directly to eliminating duplicate entry and reconciliation rework.

Every hour staff spend re-keying data is an hour they don't spend on exception handling, borrower coaching, or pipeline development. For credit unions competing with online lenders on speed and service, that gap compounds.

Integration projects live or die on whether they deliver measurable returns. Credit unions evaluating this approach should weigh three cost categories: direct labor savings from eliminating duplicate entry, error remediation costs tied to data inconsistencies that surface during audit prep, and opportunity cost for staff time that could shift to member-facing work. The labor math alone usually justifies the investment, but the opportunity cost is what shows up in member satisfaction scores six months later.

What MortgageExchange Means for Compliance and Audit Readiness

Regulators don't audit intentions. They audit data. When the same loan produces different field values across core, LOS, and servicing, examiners notice.

MortgageExchange creates a single source of truth by design. Data enters once and propagates through validated channels. Every transfer is logged. Every transformation is auditable. When NCUA or state examiners ask how a specific value moved from origination to servicing, the answer isn't "someone typed it." The answer is a timestamped integration log showing exactly what moved, when, and what validation rules it passed.

The NCUA's 2026 Supervisory Priorities letter (26-CU-01, released January 14, 2026) put this front and center for credit unions running multi-vendor stacks:

"Payment systems rely on increasingly complex integrations of applications, information systems, interfaces, security features, and internal controls. This complexity introduces the potential for added operational and security risk exposures."

The letter directs examiners to assess governance, risk assessments, vendor management, and security frameworks supporting payment-system operations, protect member data, and ensure resilience against fraud and cyber threats in the payments ecosystem. For credit unions whose data flows depend on a single staff member's recollection of which spreadsheet to update next, this is a finding waiting to happen. For credit unions running a managed integration platform with full transaction logging, the evidence shows up in the integration logs without anyone scrambling.

For credit unions under $10 billion in assets, where compliance teams are small and every examiner finding consumes disproportionate management attention, this kind of automated audit trail converts what used to be a manual documentation burden into a byproduct of normal operations.

Audit Posture Without the Scramble

An integration platform that logs every transfer turns NCUA exam prep into a query, not a reconstruction project. The reduction in manual reconciliation time is real and measurable. The reduction in examiner findings tied to data inconsistencies is the larger payoff.

Outcomes at Thrivent FCU

After deploying MortgageExchange, Thrivent reported measurable improvements across operations:

- Dual entry eliminated. The team stopped typing the same loan data into three systems and stopped fixing the preventable inconsistencies that manual entry created.

- Faster boarding and member access. Servicing setup that once waited for batch processing cycles now happens at loan milestones. Members see accurate data and get timely access to their accounts.

- Staff time redirected to higher-value work. Hours previously spent shuttling data between screens moved to borrower coaching, exception handling, and pipeline management.

- Cleaner audit posture. Consistent, validated data across all four systems means exam-ready reporting without the pre-audit scramble to reconcile discrepancies.

- A foundation that scales. Cloud-managed connectors adapt as loan volume grows or vendors evolve, without the credit union maintaining custom code.

From Thrivent FCU to Thrivent Bank

On February 6, 2025, Thrivent FCU's membership voted to approve a merger with Thrivent Bank. Roughly 33 percent of 47,872 eligible members participated in the vote, with 79 percent in favor, comfortably clearing the NCUA's 20 percent quorum threshold. The conversion took effect on June 1, 2025, and bank operations launched the following day. Thrivent Bank operates as a Utah-chartered Industrial Loan Company (ILC), shifting oversight from the NCUA to the FDIC and the Utah Department of Financial Institutions, and pivoting to a wholly digital, branchless model.

The integration work ABT built through MortgageExchange happened during Thrivent's credit union era, but the architectural principle survived the charter change. Systems that share data through a managed integration layer transfer more cleanly during organizational transitions than systems glued together with manual processes and tribal knowledge. For credit unions evaluating their own futures, whether that means organic growth, merger, or charter conversion, the lesson holds: clean data architecture isn't just an operational convenience. It's a strategic asset that holds its value through whatever comes next.

How ABT and MortgageExchange Serve Credit Unions

The strategic outcomes matter for the board presentation. But what staff actually feel is simpler than that. The LOS stopped arguing with the core. Account opening lined up with lending. Servicing started on time. The people closest to members spent their days doing the work they were hired for, because the plumbing finally worked.

For credit unions running similar swivel-chair routines across their own system stacks, Thrivent's path shows a practical principle: treat data flow as a managed service, not a project. Projects have end dates. Data keeps moving. MortgageExchange keeps it moving accurately.

Access Business Technologies is a cloud-first MSP and Tier-1 Microsoft Cloud Solution Provider serving more than 750 financial institutions. ABT's MortgageExchange platform connects LOS, core banking, account opening, and servicing systems through rules-based integration, with ongoing monitoring and connector maintenance included. The approach eliminates the "build it and forget it" risk that plagues one-time integration projects.

Ready to Stop Re-Keying the Same Loan Data?

Walk through your specific LOS, core, account opening, and servicing combination with an ABT mortgage integration specialist. We'll show you what a MortgageExchange deployment would look like, where the highest-ROI integration points are, and how examiners interpret the audit logs.

Frequently Asked Questions

MortgageExchange is a cloud-managed integration platform from Access Business Technologies that connects loan origination systems, core banking platforms, servicing software, and account-opening tools through rules-based data routing. When a loan reaches key milestones, MortgageExchange automatically pushes validated data to the right destination, eliminating manual re-entry and reducing error rates across interconnected credit union systems.

Swivel-chair integration describes the manual process where credit union staff pivot between disconnected systems to re-key the same data. Loan officers enter borrower information into the LOS, then re-type it into the core banking platform and servicing system. This creates duplicate entry, increases error rates, and consumes staff hours that could serve members directly. Jack Henry's 2025 Strategy Benchmark found 31 percent of credit unions whose tech plans fell short cited integration challenges as a primary cause.

Point-to-point integration builds direct connections between each system pair, creating maintenance complexity that grows exponentially as platforms are added. MortgageExchange uses a centralized hub with rules-based routing, so every system connects once to the platform. ABT maintains all connectors, handles vendor API changes, and monitors data flow continuously as a managed service.

MortgageExchange creates a single source of truth by validating data at the point of transfer and logging every transaction. When examiners ask how a value moved from origination to servicing, the credit union produces timestamped integration logs instead of relying on staff testimony. The NCUA's 2026 Supervisory Priorities letter (26-CU-01) specifically directs examiners to assess governance, vendor management, and security frameworks supporting payment-system operations, which is exactly what an integration log provides.

ROI depends on loan volume and current process inefficiencies, but the Mortgage Bankers Association's Q3 2025 report pegs average production cost at $11,109 per loan. Even a conservative 5 percent reduction from data-integration automation translates to roughly $555 per loan. For a credit union closing 200 loans monthly, that is approximately $111,000 per month in addressable cost reduction tied to eliminating duplicate entry, reconciliation rework, and audit prep.